DIRECT - GREAT Term

DIRECT - GREAT Term | Direct Purchase Term Life Insurance Plan

Plan your essential protection at affordable premiums

DIRECT – GREAT Term and DIRECT – GREAT 5yr Term provide essential protection against Death, Terminal Illness1 and Total and Permanent Disability2 for a fixed period at affordable premiums. These easy-to-understand plans can be bought directly with no financial advisory cost.

With DIRECT – GREAT Term, you can choose to be covered with a 20-year term plan or until age 65. Premium is guaranteed and the premium payment term will follow the chosen policy term.

With DIRECT – GREAT 5yr Term, you can have a five-year term plan renewable for the same sum assured up to age 80.

Key Benefits

-

Essential coverage at affordable premiums

Protection against Death, Terminal Illness1 and Total and Permanent Disability2

-

Choice of premium payment term to meet your needs

Choose a premium payment term of 20 years or up to age 65 or a 5-year renewable term plan.

-

Option to add-on critical illness coverage

Enhance your coverage against 30 critical illnesses with optional DIRECT - GREAT Critical Care/ 5yr Critical Care rider3 .

How to apply

You can submit an application online via "Buy Now" or visit our Customer Service Counters at Great Eastern Centre (address below):

1 Pickering Street

Great Eastern Centre

Singapore 048659

Weekday (except PH): 9:00am to 5:00pm

- Find out how much coverage you need with the Insurance Estimator: https://www.cpf.gov.sg/eSvc/Web/Schemes/InsuranceEstimator/InsuranceEstimator

- It is important to purchase an insurance plan which is within your budget. In the event that you are unable to keep up with the premium payments, your insurance policy will lapse, which will lead to a loss of insurance coverage. Check out the affordability of the premium with this calculator:

https://www.moneysense.gov.sg/financial-tools/budget-calculator

- To compare similar products in Singapore, please visit the Web Aggregator by clicking the link below:

http://www.comparefirst.sg

- Please take note of the following points before decide to purchase this plan:

(a) The DPI is not a savings account or deposit;

(b) You may not get back the premiums paid (partially or in full) if you terminate or surrender the policy early;

(c) Some benefits of the DPI are not guaranteed;

(d) There is a 14-day free-look period

- If you fulfil any two of the following criteria:

(i) 62 years of age or older

(ii) not proficient in spoken or written English

(iii) attained GCE ‘O’ level or ‘N’ level certification, or equivalent academic qualifications;

then you are strongly encouraged to bring along a Trusted Individual to our Customer Service counter to assist in your insurance application.

The Trusted Individual should be:

(i) be at least 18 years of age;

(ii) have Attained GCE ‘O’ level or ‘N’ level certification, or equivalent academic qualifications;

(iii) be proficient in spoken or written English; and

(iv) have your trust

- For information on what to expect after you purchase your plan, see view below:

Get this plan

You can submit an application by clicking on ‘Buy Now’ or for more information, please contact our friendly Customer Service Officers.

Contact us

1800 248 2888

Your questions answered

Direct Purchase Insurance Product

1. What is payable in the event of a claim?

| Type of Claim | Benefit Payable | What happens to the policy after claim is paid out? |

|---|---|---|

| Death, Terminal Illness, or Total & Permanent Disability (TPD) benefit | 100% of Sum Assured (plus attaching bonus, if applicable) will be payable in one lump sum if TPD occurs before age 65. | Policy will terminate after the claim is paid out. |

Upon Critical Illness (CI) (other than Angioplasty) |

100% of Sum Assured (plus attaching bonus, if applicable) of the main plan will be accelerated | Policy will terminate after the claim is paid out. |

Upon Critical Illness (CI) (Angioplasty) |

10% of Sum Assured (plus attaching bonus, if applicable) of the main plan will be accelerated | We will advise you of the revised premium for the reduced sum assured. |

Please refer to the Policy Contract for the exact terms and conditions.

- Suicide within one year (for Death benefit)

- Self-inflicted injury (for Total & Permanent Disability benefit)

- A waiting period (for Critical Illness benefit)

- Pre-existing medical conditions (for Critical Illness benefit)

- self-inflicted injury, while sane or insane;

- bodily injury sustained while in or on an aircraft other than

- as a fare-paying passenger or a crew member on an aircraft licensed for passenger service and operated by a regular airline on a scheduled route; or

- as a member of the armed forces travelling as a passenger in a military transport aircraft; or

- any physical or health impairment or disease which existed but was not disclosed to the Company at the date of issue of the Policy or at the date of any reinstatement.

- if there was a Pre-existing Critical Illness which is the same Critical Illness which is the subject of a claim under this Rider;

- for Heart Attack of Specified Severity, Major Cancers, Coronary Artery By-pass Surgery or Angioplasty & Other Invasive Treatment for Coronary Artery, if the diagnosis of any of these four Critical Illnesses was made within 90 days from: the date of issue of the Policy or this Rider; or the date of reinstatement of the Policy or this Rider, whichever is the later date; or

- for any Critical Illness which resulted either directly or indirectly from self-inflicted injuries of the Life Assured.

2. What are the exclusions under DPI plans?

Benefits of these plans are not payable under certain conditions. These conditions are stated in the policy contract. The categories of exclusions that are common to all life insurers relate to:

In addition to the above common categories of exclusions, all the exclusions for this plan are listed as follows:

Death Benefit

If the Life Assured dies by suicide, while sane or insane, within one year from the date of issue of this Policy or from the date of reinstatement, whichever is later, this Policy will be rendered void and the Company will refund all premiums paid to the Policyholder or to the legal personal representative of the estate of the Policyholder if the Policyholder and the Life Assured are the same person regardless of any assignment of this Policy.

TPD Benefit

Payment will not be made for TPD resulting from:

Terminal Illness Benefit

Terminal Illness in the presence of HIV infection is excluded.

Critical Illness Benefit

The Company will not pay any benefits:

The definitions of the exclusions are stated in the policy contract. Please refer to the policy contract.

3. What are the riders available?

Do note that each main plan has one corresponding Critical Illness rider that can be added. The sum assured of the rider is to be the same as the sum assured of the main plan, subject to the minimum and maximum sum assured cap.

Available riders to the corresponding Direct Purchase Insurance plans:

| Main Plan | Available Critical Illness Benefit Rider |

|---|---|

| DIRECT – GREAT Term | DIRECT – GREAT Critical Care |

| DIRECT – GREAT 5yr Term | DIRECT – GREAT 5yr Critical Care |

4. What are the minimum and maximum sum assured?

The minimum sum assured is S$50,000 (for all plans) and the maximum sum assured is S$400,000.

The maximum sum assured is applied on a per life assured, per insurer basis and is subject to underwriting by the company. The maximum sum assured is aggregated for all Direct Purchase Insurance (DPI) plans (including Term and Whole Life plans) at $400,000. In addition, on a per life assured, per insurer basis, the maximum sum assured for DPI Whole Life plans is $200,000.

For example:

- If on a per life assured, per insurer basis, a person purchases a DPI Whole Life plan which sum assured is $200,000, the person may purchase a DPI Term plan which sum assured is not more than $200,000;

- If on a per life assured, per insurer basis, a person purchases DPI Whole Life plans which aggregate sum assured is $100,000, the person may purchase DPI Term plan which aggregate sum assured is not more than $300,000;

- If on a per life assured, per insurer basis, a person purchases DPI Term plan which aggregate sum assured is $400,000, the person will not be able to purchase any DPI Whole Life;

- If on a per life assured, per insurer basis, a person purchases a DPI Whole Life plan which sum assured is $200,000, the person may only purchase a DPI Term plan which sum assured is not more than $200,000 and will not be able to purchase any other DPI Whole Life plan.

5. What are the critical illnesses (CIs) covered?

The CI Rider accelerates the payment of the basic sum assured (together with any bonuses applicable, if the main plan is a whole life plan) in one lump sum in the event that the Life Assured is diagnosed to be suffering from any one of the 30 Critical Illnesses* listed below:

| (1) Major Cancers | (16) Muscular Dystrophy |

| (2) Heart Attack of Specified Severity | (17) Parkinson’s Disease |

| (3) Stroke | (18) Surgery to Aorta |

| (4) Coronary Artery By-pass Surgery | (19) Alzheimer's Disease / Severe Dementia |

| (5) Kidney Failure | (20) Fulminant Hepatitis |

| (6) Aplastic Anaemia | (21) Motor Neurone Disease |

| (7) End Stage Lung Disease | (22) Primary Pulmonary Hypertension |

| (8) End Stage Liver Failure | (23) HIV Due to Blood Transfusion and Occupationally Acquired HIV |

| (9) Coma | (24) Benign Brain Tumour |

| (10) Deafness (Loss of Hearing) | (25) Viral Encephalitis |

| (11) Heart Valve Surgery | (26) Bacterial Meningitis |

| (12) Loss of Speech | (27) Angioplasty & Other Invasive Treatment for Coronary Artery |

| (13) Major Burns | (28) Blindness (Loss of Sight) |

| (14) Major Organ / Bone Marrow Transplantation | (29) Major Head Trauma |

| (15) Multiple Sclerosis | (30) Paralysis (Loss of Use of Limbs) |

*The Life Insurance Association Singapore (LIA) has standard Definitions for 37 severe-stage Critical Illnesses (Version 2019). These Critical Illnesses fall under Version 2019. You may refer to www.lia.org.sg for the standard Definitions (Version 2019). Definitions and details of the above Critical Illnesses are also available in the policy contract.

For Angioplasty & Other Invasive Treatment for Coronary Artery ("Angioplasty"), the basic sum assured equal to 10% of the rider sum assured (up to a maximum of S$25,000 per Life Assured) (together with any bonuses applicable, if the main plan is a whole life plan) will be payable if the Life Assured undergoes a treatment. After a claim is paid, the balance of the rider sum assured and balance of the basic sum assured with reduced premiums will continue. No benefit for Angioplasty will be payable for subsequent treatments under this and any other policies and riders covering Angioplasty.

6. What are the exclusions for Critical Illness (CI) benefit?

Benefits of this plan are not payable under certain conditions. These conditions are stated in the policy contract. The categories of exclusions that are common to all life insurers relate to:

- A waiting period (for Critical Illness benefit)

- Pre-existing medical conditions (for Critical Illness benefit)

In addition to the above common categories of exclusions, all the exclusions for this plan are listed as follows:

The Company will not pay any benefits:

- if there was a Pre-existing Critical Illness which is the same Critical Illness which is the subject of a claim under this Rider;

- for Heart Attack of Specified Severity, Major Cancers, Coronary Artery By-pass Surgery or Angioplasty & Other Invasive Treatment for Coronary Artery, if the diagnosis of any of these four Critical Illnesses was made within 90 days from:

(i) the date of issue of the Policy or this Rider; or

(ii) the date of reinstatement of the Policy or this Rider, - whichever is the later date; or

- for any Critical Illness which resulted either directly or indirectly from self-inflicted injuries of the Life Assured.

- The definitions of the exclusions are stated in the policy contract. Please refer to the policy contract.

7. Can I make changes to the CI rider after my policy turns inforce?

The CI rider may be cancelled after policy turns inforce.

1. Does Great Eastern have a panel of doctors?

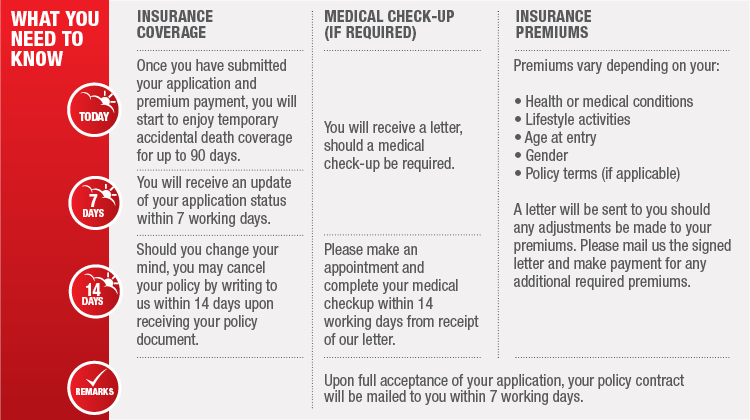

Yes, the Company has a panel of doctors. The list would be provided should medical check-up is required.

2. Do I have to pay for the medical check-up?

You do not have to pay for the medical check-up which is requested by the company. However, should you decide to free-look the policy, the cost of the medical check-up will be deducted before refund of premiums.

3. What if I change my mind about the new policy, i.e. how to freelook my policy?

This Policy may be cancelled by written request to the Company within 14 days after the Policyholder has received the policy document in which case premiums paid less medical fees (if applicable) incurred in assessing the risk under this Policy will be refunded.

If this policy document is sent by post, it is deemed to have been delivered and received in the ordinary course of the post 7 days after the date of posting.

Please refer to “Your Servicing Guide” attached for more information.

1. How do you inform me when premium is due?

You will not receive premium notices if you are paying by monthly mode. For all other modes of payment, premium notices will be mailed to you.

2. What are the different payment methods available?

Please refer to “Your Servicing Guide” or our website for more details on payment methods available for your policy.

3. What is the GIRO deduction date?

Once your GIRO application is approved by your designated bank, you will receive a confirmation letter to advise you on the pre-assigned GIRO deduction date for your policy(ies).

4. Will I receive any receipt after I pay my renewal premium?

An official receipt will be mailed to the policyholder upon receipt of the payment of renewal premium. No receipt will be issued for payment via GIRO or credit card.

5. How do I change my payment frequency?

Yes, you may download the Application for Change Form from our website and complete “Section 1: Change of Payment Frequency” and post it to us.

6. What are the risks if I do not pay the premiums on time?

| Type of Plans | What will happen to my policy? |

|---|---|

| Term Plans | If premiums are not paid on time, your policy will lapse (after 30 days grace period). However, reinstatement of the policy is allowed within 6 months from the lapse date and usual reinstatement conditions apply. |

| Whole Life Plans | If premiums are not paid on time, your Policy may lapse (after 30 days grace period) depending on the net surrender value. If the Policy has sufficient net surrender value, an automatic premium loan (APL) will be granted. If the Policy lapses due to insufficient net surrender value, reinstatement of the Policy is allowed within 3 years from the lapse date and usual reinstatement conditions apply. |

7. What is the penalty for early termination of policy?

If you cancel your Policy within the free-look period i.e. 14 days from receiving your policy document, you will get a refund of your premiums paid less any medical fees. If you surrender your Policy after the free-look period, you may lose part or all of the premiums paid as the surrender value payable, if any, may be less than the total premiums paid. Purchasing a new policy may require underwriting and may result in higher premiums and/or benefit exclusions due to your age and health status at the point of re-application.

1. How do I submit a claim?

You may download and print the claim forms from our Great Eastern website at www.greateasternlife.com

- Click on “Quick Links” and select “Submit a Claim”. Choose the relevant form you need from the list, and print it.

- Fill in the required forms and ask your doctor to complete the doctor’s statement.

- Submit all the required forms and supporting documents to us for assessment.

2. How do I check my claims status? You may check on the status of your submitted claim through any of these options:

- Log on to e-Connect for online information about your policies.

- Email us at LifePAClaims-SG@greateasternlife.com. You may check on the status of your submitted claim through any of these options

Let us match you with a qualified financial representative

Our financial representative will answer any questions you may have about our products and planning.

Understand the details before buying

1 Terminal Illness refers to a conclusive diagnosis of an illness that is expected to result in the death of the Life Assured within 12 months of the diagnosis. The terminal illness must be diagnosed by a registered medical practitioner and must be supported by evidence acceptable to the Company. Please refer to the policy contract for the full list of exclusions.

2 Total and Permanent Disability (TPD) refers to:

(a) The Life Assured, due to accident or sickness, is disabled to such an extent as to be rendered totally unable to engage in any occupation, business or activity for income, remuneration or profit; and the disability must continue uninterrupted for at least 6 consecutive months from the time when the disability started; and the disability must, in the view of a medical examiner appointed by the Company, be deemed permanent with no possibility of improvement in the foreseeable future; or

(b) The Life Assured, due to accident or sickness, suffers total and irrecoverable loss of use of:

(i) the entire sight in both eyes; or (ii) any two limbs at or above the wrist or ankle; or (iii) the entire sight in one eye and any one limb at or above the wrist or ankle.

Subject to a maximum TPD Benefit of S$5,000,000 on all policies and riders issued by the Company on the same Life Assured.

The TPD benefit is only applicable if TPD occurs before the policy anniversary on which the Life Assured is age 65 next birthday.

3 DIRECT - GREAT Critical Care/ 5yr Critical Care rider. On diagnosis of one of the 30 critical illnesses (except for Angioplasty & Other Invasive Treatment for Coronary Artery), the basic sum assured will be accelerated and paid in one lump sum. This rider will then be terminated. The amount of accelerated basic sum assured equals to the sum assured of this rider.

Subject to a maximum CI Benefit of S$3,000,000 on all policies and riders issued by the Company on the same Life Assured.

For Angioplasty & Other Invasive Treatment for Coronary Artery (“Angioplasty”), the basic sum assured equal to 10% of the rider sum assured (up to a maximum of S$25,000 per Life Assured) will be payable if the Life Assured undergoes a treatment. After a claim is paid, the balance of the rider sum assured and balance of the basic sum assured with reduced premiums will continue. No benefit for Angioplasty will be payable for subsequent treatments under this and any other policies and riders covering Angioplasty.

No benefit under this rider will be payable for Heart Attack of Specified Severity, Major Cancer, Coronary Artery By-pass Surgery or Angioplasty & Other Invasive Treatment for Coronary Artery if the diagnosis is made within 90 days from the date of commencement of this rider, or from the date of any reinstatement.

Sum assured is capped at S$400,000 for all direct purchase insurance plans.

There are two non-participating riders available:

- You can attach DIRECT – GREAT Critical Care to DIRECT – GREAT Term.

- You can attach DIRECT – GREAT 5yr Critical Care to DIRECT – GREAT 5yr Term.

Premiums vary according to age at entry, gender and lifestyle choices, such as smoking. The premium charged is not guaranteed and may be revised in future at the Company’s discretion

All ages specified refer to age next birthday.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The above is for general information only. It is not a contract of insurance. The precise terms and conditions of this insurance plan are specified in the policy contract.

As this product has no savings or investment feature, there is no cash value if the policy ends or is terminated prematurely.

As DIRECT - GREAT Term is a Direct Purchase Insurance plan, you can sign up for it directly without seeking any advice from any financial advisory representative.

These policies are protected under the Policy Owners' Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC websites (www.lia.org.sg or www.sdic.org.sg).

In case of discrepancy between the English and the Chinese versions, the English version shall prevail.

Information correct as at 29 June 2021.