BRANDED CONTENT

Financial support and income replacement: How cancer patients can have better peace of mind

Critical illness insurance can relieve money worries and help patients focus on recovery

Critical illness insurance helps give patients peace of mind as it can help with their ongoing expenses and replace potential loss of income. PHOTO: GETTY IMAGES

Mr Joel Lim was 26 when he was diagnosed with pancreatic cancer in 2016.

He underwent surgery to remove a tumour in the pancreas, and followed up with chemotherapy. Three years later, in 2019, doctors told him the disease has progressed to stage 4, meaning cancer has spread to other parts of the body.

Thanks to advances in cancer treatments, including newer treatments such as immunotherapy that activates the body's immune system to fight the disease, he has managed to defy the initial poor prognosis. But these new treatments come with a hefty price tag.

Mr Lim estimates that the recent radiotherapy treatments have so far added up to about $30,000, while his twice-monthly immunotherapy treatments cost close to five-figures each month and these treatments are still ongoing. His surgery in 2016 cost a six-figure sum.

Thankfully, his hospitalisation insurance plan covered most of his medical expenses. A former financial representative, he also has critical illness, life and personal accident policies.

“I was lucky that I had insurance coverage before I was diagnosed with pancreatic cancer,” he says. “Without insurance, the sum I would have had to fork out would have been unimaginable. But my treatment costs have been almost fully paid for by my hospitalisation plan, which I think is pretty awesome.”

While payouts from his hospitalisation plans covered the bulk of his medical bills, the lump-sum cash paid out from his critical illness and whole life plans, offered Mr Lim and his family valuable additional financial support as income replacement during the four years while he took a break from working to recuperate.

“After I was diagnosed, I wasn’t able to work, so the money came in handy to help out with my family’s day-to-day expenses and my own living expenses. We also use part of the cash to pay for my brother’s tuition fees and his pilot course fees to get him to where he is today,” he says.

“Without insurance, the sum I would have had to fork out would have been unimaginable.”

Mr Joel Lim, 32

Like Mr Lim, cancer patients often feel that their world has been turned upside down when they first receive the cancer diagnosis. Besides having to deal with their own emotional distress, many are also worried about their families and whether they can continue to provide for their dependents.

For 64-year-old Eddie Low, his worst fears would be to become a burden to his only daughter, who is now in her thirties and married with a child.

He was diagnosed with lung cancer five years ago, in 2017, while undergoing a routine checkup. A year later, he was diagnosed with liver cancer and prostate cancer. Between 2017 and 2020, he underwent multiple procedures, including keyhole surgery on his liver, chemotherapy to treat lung cancer and radiotherapy to treat prostate cancer.

His medical bill added up to roughly $400,000.

“Singapore Cancer Society’s programmes and support groups, helped me overcome some of the physical and emotional challenges that I faced during my journey to recovery. These included the SCS Return to Role programme, workshops on nutrition and mental wellness as well as rehabilitative exercises which helped strengthen my body, and helped me cope in this journey.”

Critical illness can strike at any time

Cancer is the number one cause of death in Singapore, accounting for 28.4 per cent of all deaths in the country.

But with early detection and advances in cancer treatment, a cancer diagnosis is not a death sentence.

Dr Richard Quek, senior medical oncologist at Parkway Cancer Centre, says that treatment pathways and costs can vary greatly.

“Treatment depends on cancer type, stage, location, modalities of treatment required. Thus, treatment cost is also highly variable depending on what treatment is required,” he says.

One thing is certain though: Treatment cost is increasing every year. And even when a patient is in remission, there is always the fear of a recurrence. Recurrence rates can vary significantly depending on the type of cancer, but can be as high as 85 per cent in the case of ovarian cancer .

Other than cancer, critical illnesses like stroke are amongst the top leading causes of death in Singapore.

“Like any other critical illness, stroke can be caught in the early stage, which is known as transient ischaemic attack. This is a warning sign that a stroke may occur in the future. Statistics have also shown stroke has a recurrence rate of up to 18 per cent ,” says Dr Chou Ning, a neurosurgeon at Chou Neuroscience Clinic.

Mr Lim says that the payouts he received from his insurance plans took a big load off his mind, allowing him to focus on the treatments to fight cancer.

“When I realised that the hospitalisation costs were covered and the critical illness plan paid out just fine, it was really a huge sigh of relief.”

He urges more young people to get the protection they need before it is too late.

“It’s only when such incidents happen that they realise they should have been better prepared for life’s unforeseeable events,” he says.

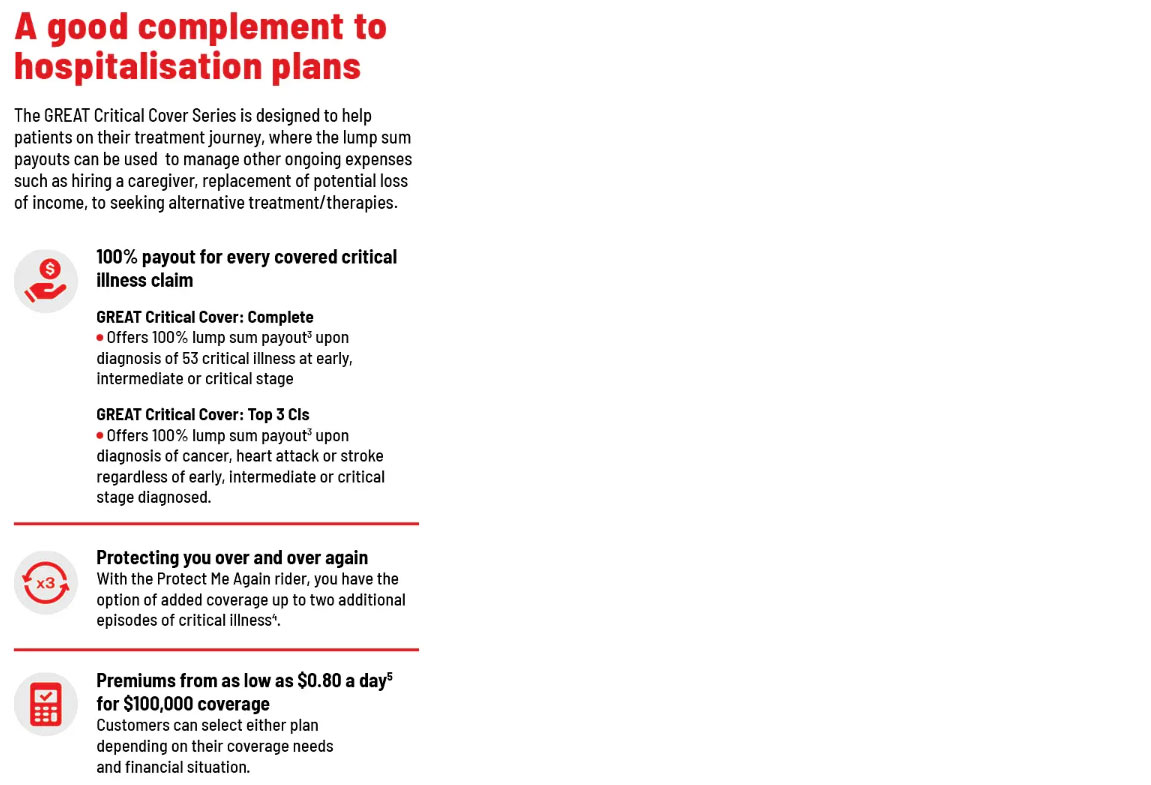

Visit this website to find out more about Great Eastern’s GREAT Critical Cover Series.

1 https://www.cancertherapyadvisor.com/home/tools/fact-sheets/cancer-recurrence-statistics/ 2https://bmcneurol.biomedcentral.com/articles/10.1186/1471-2377-13-133 3Please refer to the Product Summary for more details on the benefit terms and conditions. 4Coverage restores to 100% after 12 months from the date of diagnosis for the most recently diagnosed critical illness, for a subsequent claim of a different critical illness. Coverage restores to 100% after 24 months from the date of diagnosis of the immediately preceding applicable critical illness for recurrent critical illness. Please refer to the Product Summary for more details on the benefit terms and conditions. 5Annual premium of S$278.30 for the first year after the 30% first-year discount, is based on a 30-year-old male, non-smoker. The daily rate is based on a 30-year-old male, non-smoker with the annual premium of GREAT Critical Cover: Top 3 CIs and Protect Me Again rider for a sum assured of S$100,000 and policy term of up to age 85, divided by 365 days and rounded off to the nearest 1 decimal place. The annual premium will increase based on the attained age of the life assured, as at each policy anniversary. Premium rates are not guaranteed and may be revised based on future experience.

This advertisement has not been reviewed by the Monetary Authority of Singapore. The above is for general information only. It is not a contract of insurance. The precise terms and conditions of this insurance plan are specified in the policy contract. As this product has no savings or investment feature, there is no cash value if the policy ends or is terminated prematurely. You may wish to seek advice from a financial adviser before making a commitment to purchase this product. If you choose not to seek advice from a financial adviser, you should consider whether this product is suitable for you. Protected up to specified limits by SDIC. Information correct as at Oct 16, 2022.

This article was first published in The Sunday Times on 16 October 2022.