Integrated Shield riders: Fresh focus on cancer drug cover, brace for premium hikes

IP riders now have additional cancer drug benefits far more than the base plans, raising the question of whether current premiums are sustainable

By Genevieve Cua

RIDERS to supplement private Integrated Shield Plans (IPs) are set to take on new significance for policyholders, particularly if you are concerned about the extent of cancer drug coverage.

The big question is – are today’s rider premiums sustainable given the riders’ enlarged role in outpatient cancer cover?

Insurers in the IP scheme recently rolled out their base IP plans and riders, with reference to the caps for cancer drug coverage, in line with the cancer drug list (CDL) issued by the health ministry last year.

The list is part of a major effort to rein in the escalating cost of cancer treatments. It comprises cancer drugs which satisfy two criteria – they are clinically proven and cost effective.

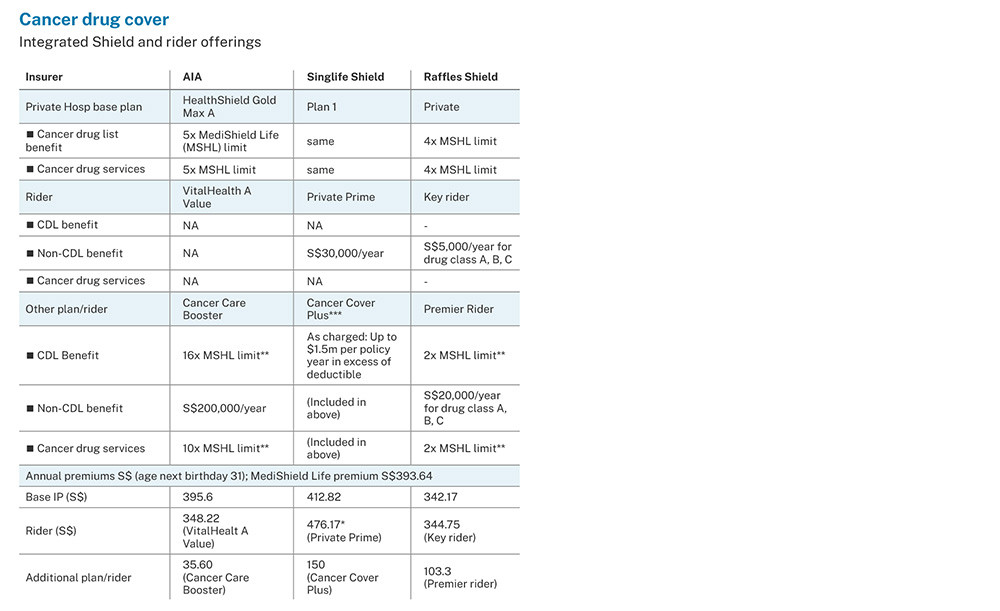

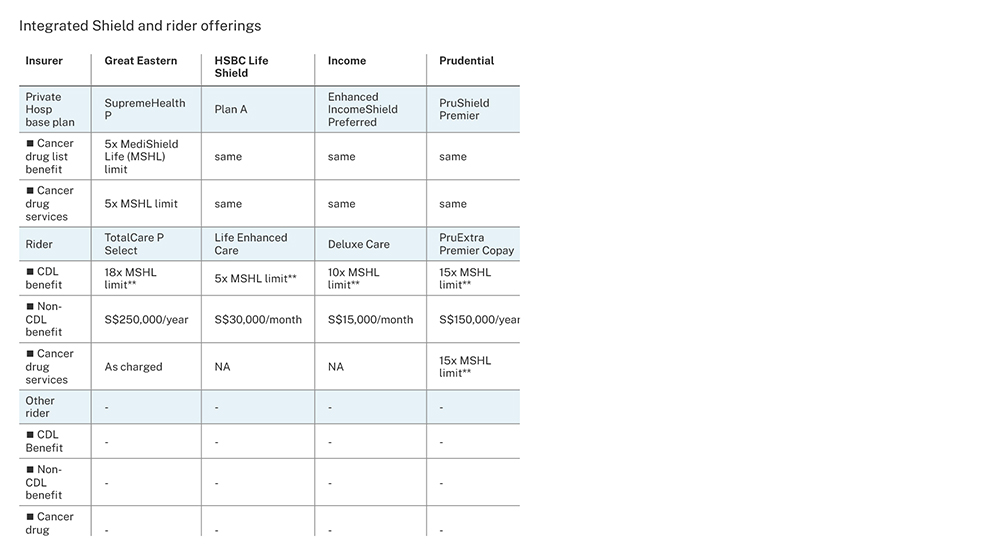

MediShield Life revised its cancer drug coverage in September 2022 to exclude drugs not on the list. IPs were required to comply in April this year. Previously, IP base plans for private hospitals covered outpatient cancer charges on an “as charged’’ basis. Most IPs for private hospitals now offer a benefit of five times the MediShield Life limit for outpatient cancer treatment.

MediShield Life’s limit is between S$200 and S$9,600 a month. At a multiple of five times, an IP base plan may cover between S$1,000 and S$48,000 a month for CDL drugs. There is also an annual limit on cancer drug services, which include consultations and lab investigations.

But attention is now focused on IP riders, where insurers have chosen to cover non-CDL cancer treatments, on top of an even greater multiple of the base plans’ cover for CDL drugs and services.

Two insurers – AIA and Singlife – have opted to offer separate riders for outpatient cancer benefits. AIA’s Max A Cancer Care Booster offers 16 times the Medishield Life limit per month for CDL drugs – on top of the limit of up to five times in the base plan. This makes a maximum cover of up to 21 times. There is also an annual limit of S$200,000 for non-CDL drugs.

Singlife’s Cancer Cover Plus offers up to S$1.5 million in benefit per year for CDL and non-CDL treatments, in excess of the deductible.

Overall, the rider offerings add a wrinkle to the IP landscape. Previously, riders were mainly designed to cover the deductible and co-insurance portions of bills. Policyholders have suffered frequent premium hikes for both IP base plans and riders, because a base plan which covers bills on an “as charged” basis – coupled with a rider – will enlarge claims.

To save costs, some policyholders may choose to forego riders and self-insure the deductible and co-insurance portion of bills. But that calculus has shifted as riders rise in importance for outpatient cancer cover.

Premium hikes for riders will, of course, depend on insurers’ claims experience. Factors which can mitigate the size of claims include caps on CDL and non-CDL drugs, and the use of panel doctors. Some insurers also have a system of claims-based pricing, which applies a discount for those who don’t claim, and adjusts premiums upwards for those who do.

Eddy Cheong, Providend’s head of solutions, said: “With the latest IP changes to restrict cancer cover, the rider is not just to cover the smaller ticket but also potentially larger out-of-pocket expenses from cancer treatments, especially for non-CDL. Hence, having an IP rider that covers cancer treatment is becoming important from a risk mitigation standpoint, especially for private hospitals.

“This is less so for public hospital plans as cancer drugs in public hospitals are much cheaper than private. But if one can afford it, it seems to make financial sense to get the rider too.”

Last year, insurers gave the undertaking not to raise premiums for IP base plans for two years until end-August 2024. There is no such undertaking for riders.

Health Minister Ong Ye Kung has said that the health ministry has no objections to insurers covering treatments not on the CDL. Premiums, he said, will reflect the additional coverage.

Unbundling the cancer benefit into a separate optional rider may ultimately offer more flexibility, particularly if affordability becomes an issue at older ages.

According to Life Insurance Association (LIA) data, 2.89 million lives – 70 per cent of Singapore residents – are covered by IPs and IP riders. Of those who hold IPs, about two-thirds have riders.

Providend’s Cheong says: “(Unbundling) might be a better way to give choices to consumers to allow them to decide what is covered – coinsurance/deductible, cancer benefits or both – and a better pricing approach for individual riders.’‘

Of the riders in the market, Singlife’s optional Cancer Cover Plus with its annual limit of S$1.5 million is effectively an as-charged plan for outpatient cancer cover. Singlife says that treatment for certain late-stage cancers can range in the hundreds of thousands of dollars, and existing insurance plans alone are “wholly insufficient’’ to cover the cost.

The rider is expected to reduce out-of-pocket expenses by up to 88 per cent for clients who hold the firm’s private hospital base plan.

According to Cheong, Singlife’s Cancer Cover Plus appears to be designed to cover “extreme’’ costs of cancer treatments. “It depends on how far you want to go for cancer protection. If your IP rider has a good cover for cancer benefit, then that might suffice. As this adds to your insurance budget, you should consider if it is well within your means.”

Great Eastern’s benefit is the most generous among insurers who have opted to add on the CDL and non-CDL benefits onto existing riders. For its private hospital rider, the CDL benefit is effectively 23 times the MediShield limit.

The cap of S$250,000 for non-CDL drugs is expected to cover almost three times GE’s maximum outpatient chemotherapy bill of S$92,213, based on its 2022 claims data. Its average chemotherapy bill was far lower at S$6,074.

Eddy Lim, GE head of products and propositions, says that the firm’s offering is highly competitive in terms of value and affordability. “The higher limits offer greater peace of mind as they significantly lower the chances of large out-of-pocket bills… We will continue to monitor our customers’ cancer treatment bills closely to assess if our plan meets their needs comfortably.’’

Here are some things to note:

- Coverage for non-CDL drugs are subject to a “non-CDL classification framework’’ which can be found on the LIA website. Insurers may choose to exclude certain classes of treatments.

- For those who already hold IP riders, there is typically no underwriting for the additional outpatient cancer benefits.

- A co-insurance charge may apply to the riders’ outpatient cancer benefit.

Source: The Business Times © SPH Media Limited. Permission required for reproduction.

This article was first published in The Business Times on 17 April 2023.