Should I get covered for long-term disability?

Disability doesn’t just affect the old. It can happen due to an accident or an unexpected illness.

When I was younger (in my 20s), I used to think that disability only happened to the elderly. But apparently that couldn't be further from the truth, as there are 3 main causes of disability in Singapore - accidents, illness or old age1 - and the first two can happen to anyone regardless of age.

And that was when I realised, just like how even the healthiest of people can suddenly get stricken with cancer, anyone can also suddenly become disabled if you're unfortunate.

- 2 young men in their 20s ended up becoming 100% reliant on a caregiver2, despite them being at an age where you least expect disability to happen. One got into a road accident while another fell, and both ended up permanently disabled for life.

- This woman in her 30s, who is now in a nursing home for long-term care after she was left permanently disabled when a bus hit the bicycle she was riding on.

It will be hard enough to pick yourself up should disability happen, but if one also faces financial difficulties in doing so, I can imagine it'll be even more stressful - not just for the victim, but for their loved ones as well, as they may now have to be the primary caregiver, foot the additional expenses, and even possibly become the sole breadwinner from there on.

Which is why my husband and I had a detailed discussion about this recently. We did a review of our household expenses (now that we have welcomed our second child) and realised that if one of us were to stop contributing our income, then we would soon be in trouble as our emergency funds can only last us up to one year of expenses.

So now that we have our basics (health, life, critical illness) covered, we’ve been seriously discussing about taking up more coverage against disability.

Use insurance to protect against the risks that you cannot plan for

With 7 dependants to support, my husband and I cannot afford to let any unexpected event(s) leave a dent in our finances. In fact, our finances are so prudently planned out that any major and unexpected hit may just derail our entire plan for our kids, parents’ retirement and that of our own.

This is why we're huge believers of using insurance to protect against the risks that we cannot plan for.

And in this case, disability is definitely a very real risk not to be taken lightly.

Is disability insurance necessary?

These might help you to judge for yourself:

- This 19-year-old Singaporean certainly didn't expect to suffer a stroke at such a young age, and it took an entire year of recovery before he was able to walk on his own3.

- In Singapore, there has been more than a 20% increase in the number of stroke patients aged 15 - 49 years old, with a significant increase in the 15 - 29 age group4.

- The lifetime impact of a stroke also carries substantial costs to the victims and their families, with some still unable to function independently even after 10 years.

You should also probably ask yourself these questions:

- Do you have enough savings to pay for inflation-adjusted long-term care costs (such as medical and caregiving expenses)?

- What if you lose your income due to disability?

- Would your loved ones have to pick up the financial pieces? What if your children are still young and schooling?

Many people take their health and physical mobility for granted, but the truth is, accidents and illnesses are the most common causes of disabilities in Singapore for the younger folks. One could be knocked down while walking on the pavement thanks to an errant rider, or get into a car crash (not your fault, obviously), or even suffer a sudden stroke with no warning signs at all.

In fact, based on a local 2015 NCSS sample, the prevalence rate of folks aged 18 - 49 with disabilities is over 3 in 100†.

That's why we're now looking into 2 plans: severe disability (loss of any ADL) and income replacement, and in that order too.

In this article, I outline our thought process for the first.

Won't CareShield Life be enough?

In my view, CareShield Life is and will not be enough.

Based on the current payout level of $612 a month, this amount is already insufficient for food and transport, what more for medication and rehab treatments.

The cost of hiring a foreign domestic worker today is already minimally ~$700 a month, assuming you qualify for the levy concession ($60 instead of $300)‡. Good helpers with experience will typically cost more.

If a stay in a nursing home is required, it can easily go up to several thousand dollars a month5.

As with most national insurance schemes, I feel they serve as a good basic foundation, but it is also our own responsibility to supplement it with private insurance and/or proper financial planning.

The question to ask yourself here is, will $600 in today's terms be enough for you?

If your answer is no (just like us), then you should probably look seriously into adding on further protection.

How much do I need?

Start by estimating how much you need based on long-term care costs for disability. Paying for a caregiver, medical treatments (especially those that fall outside of your hospitalisation insurance) and rehab ought to be included in your calculations.

Alternatively, you can try out Great Eastern’s disability calculator here to estimate how much you might need:

Depending on your lifestyle and the extent of your disability, you may or may not need more than just that.

For us, aside from wanting to cover both a loss of income and long-term care costs, we also value a plan that can help us from as early as the onset of inability to perform 1 ADL, so that we can gain early access to treatments and rehabilitation care that can potentially help with an earlier recovery.

And since we have so many dependants who rely on our income, it makes almost no sense for one spouse to become the primary caregiver rather than going out to work and earn more money to make up for the other half's income loss. That's why having additional benefits to help support both a caregiver and our dependants are preferred.

While some insurers offer payouts of up to $5,000 a month, we decided to go with $2,000 each for ourselves for now, which will hopefully be sufficient to pay for long-term care costs on a prudent lifestyle. In the event that costs rise faster than we predicted, we may consider adding on further coverage at a later stage.

Review of GREAT CareShield

We did our research and I arranged for a discussion with my Great Eastern Financial Representative to find out more.

Here's what we like:

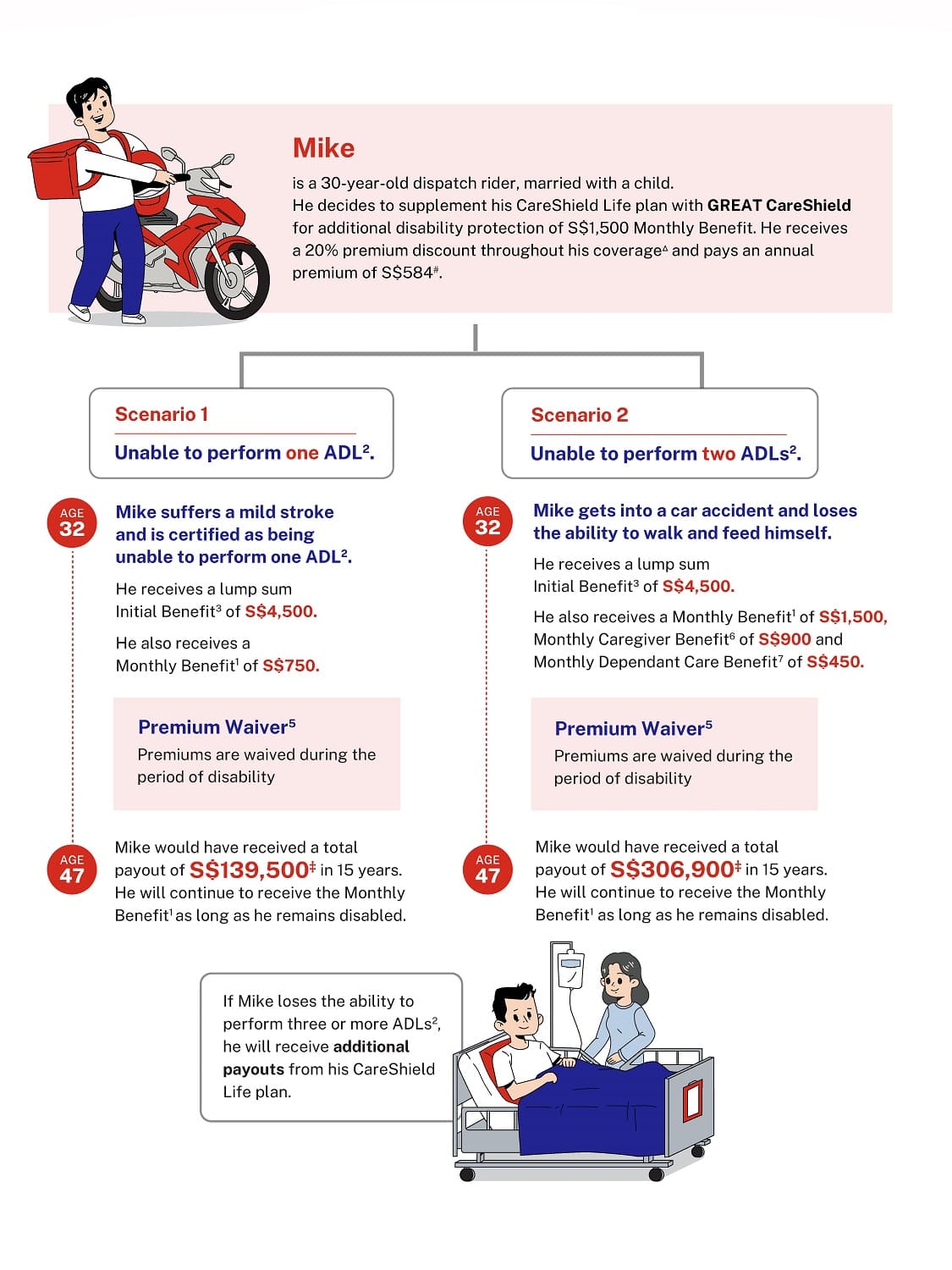

- Financial support starts from the inability to perform 1 ADL, with a lump-sum Initial Benefit* (up to S$15,000) and 50% of Monthly Benefit* * (up to S$2,500) paid out. Your future premiums will also be waived^. The initial lump-sum benefit is also payable again upon future occurrence of disability from a different cause. This is currently unique to Great Eastern as none of the other insurers offers it.

- Caregiver Benefit^^ of 60% monthly benefit (upon 2 ADLs) for up to 12 months, to help with the adjustment period. This means you can get up to S$3,000, depending on your monthly benefit level.

- Dependant Care Benefit*^ of 30% monthly benefit if you have a child under 22 at the time of claim (upon 2 ADLs) for up to 48 months i.e. 4 years of support. This means you can get up to S$1,500, making it highest in the market right now.

I'm not able to compare like-for-like across all the other insurers, because the payment terms differ (e.g. pay until age 62/95 vs. 67/99) but surprisingly, the premiums for Great Eastern are very affordable.

| For $1,200 Monthly Benefit | Pay until age 67 | Pay until age 95 |

| 30-year-old Male | $692.59 | $467.74 |

| 30-year-old Female | $848.63 | $623.92 |

| 45-year-old Male | $1,556.00 | $840.26 |

| 45-year-old Female | $1,913.87 | $1,134.95 |

Figures are valid as of 1 January 2024 and after factoring in the 20% off premium discount + GST.

You can use up to S$600 each year from your MediSave^* to pay for the premiums, meaning that depending on your chosen Monthly Benefit (a.k.a. monthly payout in the event of disability to perform at least 2 ADLs) and premium term (whether you wish to pay until age 67 or 95), there is a chance that you may not even have to fork out any extra cash to get this protection.

In our case, although we pay premiums on an annual basis, the premiums for a Monthly Benefit of S$2,000 works out to be about S$30 (for my husband) and S$35 (for me) in cash expenses each month.

Which I feel is very affordable, and something we're definitely willing to pay for.

Conclusion

Disability can happen to anyone regardless of age and marital status, so it is definitely important to get yourself insured for it. I believe I'm not the only one who feels the payouts from CareShield Life won't be enough.

If budget is an issue, you can always adjust your coverage level to what you can afford for now, and look at adding on more later when your finances improve.

That way, if anything unfortunate were to happen, at least you won't become a liability to your loved ones, and have the finances to at least get through the ordeal.

Great Eastern's GREAT CareShield looks like a good option right now for us, but regardless of which plan you pick, the more important message in this article is to get yourself covered for what you may need.

Sponsor's Message

Enjoy 20% off premiums throughout your GREAT CareShield coverage when you sign up. Click here for more information.

Terms and conditions apply.

Disclosure: This post is sponsored by Great Eastern. All opinions are that of my own, and information accurate as of 1 January 2024.

Source:

1 Ministry of Social and Family Development, Total Number Of Persons With Disabilities In Singapore (2018).

2 True grit: Paralysed after separate accidents. https://www.todayonline.com/singapore/true-grit-paralysed-separate-accidents-two-men-fight-on-to-live-fully

3 Massive stroke at 19: 'This doesn't happen to someone my age'. https://www.straitstimes.com/singapore/massive-stroke-at-19-this-doesnt-happen-to-someone-my-age

4 Can Stroke Affect The Young? https://www.jaga-me.com/thecareissue/can-stroke-affect-the-young/

5 Introduction To Nursing Homes. https://www.aic.sg/care-services/nursing-home

† Ministry of Social and Family Development, Total Number Of Persons With Disabilities In Singapore (2018).

‡ Introduction To Foreign Domestic Worker (FDW) Levy Concession For Persons With Disabilities. https://www.aic.sg/financial-assistance/foreign-domestic-worker-levy-concession

Footnotes:

* Subject to Deferment Period. The Initial Benefit is a lump sum payment equivalent to 3 times of the Monthly Benefit. In the event the Life Assured fully recovers from the disability, the Initial Benefit may be paid again for subsequent episodes of inability to perform at least 1 ADL. However, it is not payable if such subsequent disabilities arise from or are related to the cause of disability(ies) for which there was a previous claim for Initial Benefit.

**Subject to Deferment Period. Payouts of Monthly Benefit are payable for as long as the Life Assured suffers from the applicable number of disabilities, up to a lifetime. The payouts will be increased to 100% of the Monthly Benefit (up to $5,000) upon disability to perform at least 2 ADLs.

^ Subject to Deferment Period, and for as long as the Life Assured continues to suffer from the disability.

^^ Subject to Deferment Period and payable for up to a maximum of 12 months (whether consecutive or not) per Policy Term.

*^ Applicable if the Life Assured has a Child who is below 22 years old (age last birthday) as at the Claim Date; subject to Deferment Period and payable for up to a maximum of 48 months (whether consecutive or not) per Policy Term.

^* Subject to cap of S$600 per calendar year per insured person.

Disclaimers:

This comparison does not include information on all similar products. Great Eastern does not guarantee that all aspects of the products have been illustrated. You may wish to conduct your own comparison for similar products. For more information, you can refer to www.careshieldlife.gov.sg.

The information presented is for general information only and does not have regard to the specific investment objectives, financial situation or particular needs of any particular person.

All ages specified refer to age last birthday.

Figures illustrated (except figures in premium table) are rounded down to the nearest dollar.

The above is for general information only. It is not a contract of insurance. The precise terms and conditions of this insurance plan are specified in the policy contract.

GREAT CareShield can be purchased by CareShield Life or ElderShield policyholders. All Supplements are regulated under the CareShield Life and Long-Term Care Act 2019.

This is only product information provided by us. You may wish to seek advice from a qualified adviser before buying the product. If you choose not to seek advice from a qualified adviser, you should consider whether the product is suitable for you. Buying health insurance products that are not suitable for you may impact your ability to finance your future healthcare needs.

If you decide that the policy is not suitable after purchasing the policy, you may terminate the policy in accordance with the free-look provision, if any, and the insurer may recover from you any expense incurred by the insurer in underwriting the policy.

Protected up to specified limits by SDIC.

Information is correct as at 1 January 2024.

Let us match you with a qualified financial representative

Our financial representative will answer any questions you may have about our products and planning.