Unlock tax savings with the SRS

What exactly is the Supplementary Retirement Scheme (SRS)?

The Supplementary Retirement Scheme (SRS) is part of Singapore's Government’s policy for Singaporeans, Singapore Permanent Residents (PR), and foreigners to save for retirement needs.

In contrast to CPF contributions which are mandatory, contributions towards SRS are voluntary. Contributions into your SRS account are over and above your CPF savings, and are eligible for tax relief.

Save on your taxes. Accumulate more for your golden years.

Every year, you can choose to contribute funds into your SRS account which may be used to purchase various investment instruments to potentially earn higher returns for your retirement. Investment returns are tax-free before withdrawal and only 50% of the withdrawals from SRS are taxable on or after your statutory retirement age.

How it works

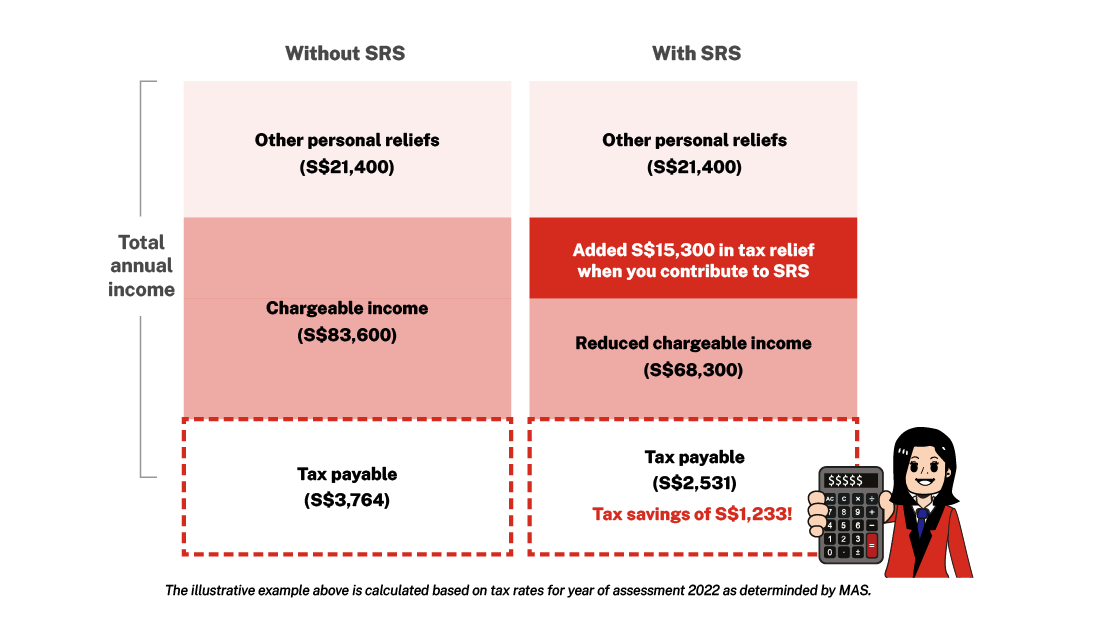

The following illustration is based on an individual's annual income of S$105,000 and a personal relief of S$21,400.

Get a dollar-for-dollar tax relief on your yearly income with every dollar saved into your SRS account. Work out how the yearly maximum SRS contribution of S$15,300 can help reduce your tax payment:

Using SRS for retirement

It’s never too early to start thinking about retirement. While SRS may be labelled as a retirement scheme, you can get started from 18 years old to open a SRS account with one of the 3 bank operators in Singapore:

- DBS Group Holdings Ltd

- Oversea-Chinese Banking Corporation Ltd

- United Overseas Bank Ltd

Funds from your SRS account can be used to invest in various financial products such as exchange traded funds, local shares, bonds, unit trusts or insurance products.

Benefits for investing using SRS

- Enjoy tax relief for every dollar saved into the account, plus benefit from lower tax payable.

- Freedom to invest SRS to boost retirement savings.

- Only 50% of withdrawals are taxable after retirement.

Our range of insurance plans available that can help maximise the growth potential of your SRS funds:

- GREAT Wealth Multiplier 3 (Single Premium)

- GREAT Prime Rewards 3

- GREAT Invest Advantage

- Prestige Portfolio

- GREAT SP Series (limited period tranche)

Here's how GREAT Wealth Multiplier 3 can potentially multiply and boost your SRS

Enjoy potential tax savings on your SRS contributions as you optimise your wealth with us. What’s more, receive added insurance coverage for greater peace of mind.

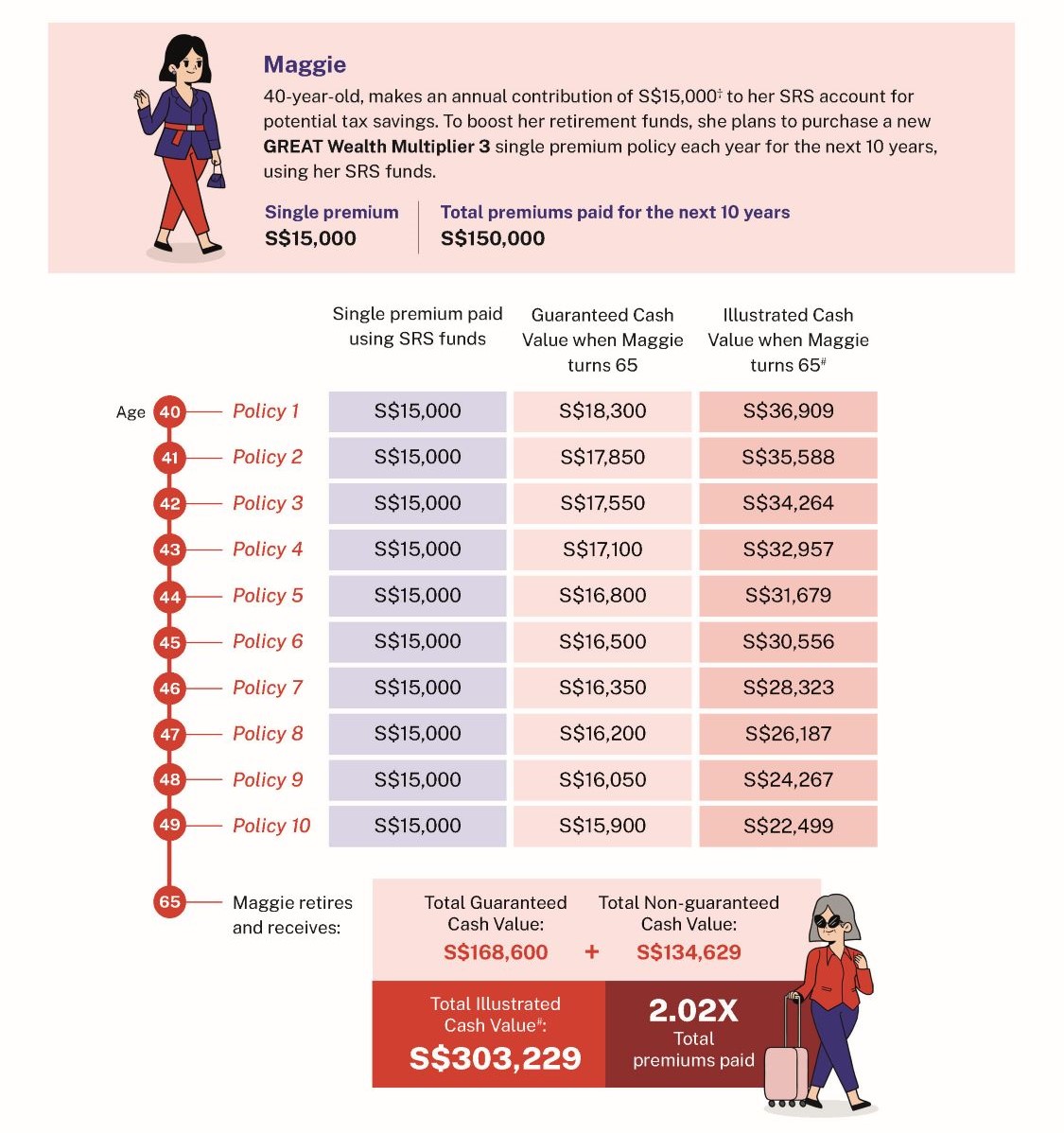

Here’s an illustration of how Maggie uses her SRS funds with GREAT Wealth Multiplier 3.

Speak to our experienced Financial Representative to find out how you can optimise your SRS funds to boost your retirement savings.

Footnotes

† For Singapore Citizens and Singapore Permanent Residents, the yearly maximum SRS contribution is S$15,300. For foreigners, the yearly maximum SRS contribution is S$35,700. Please refer to the Inland Revenue Authority of Singapore’s (IRAS) website for more details.

# The figure comprises guaranteed and non-guaranteed benefits. The non-guaranteed benefits are illustrated based on an IIRR of the participating fund at 4.25% p.a.. Based on an IIRR of 3.00% p.a., the illustrated cash values when Maggie turns 65 are S$26,007, S$25,193, S$24,472, S$23,671, S$22,969, S$22,331, S$21,351, S$20,418, S$19,569, and S$18,773. The total illustrated cash value is S$224,754 (1.49X of total premiums paid). The actual benefits payable may vary according to the future performance of the participating fund.

Disclaimers

All ages specified refer to age next birthday.

All figures used are for illustrative purposes only and are subject to rounding.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The above is for general information only. It is not a contract of insurance. The precise terms and conditions of this insurance plan are specified in the policy contract.

As buying a life insurance policy is a long-term commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid.

This policy is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC websites (www.lia.org.sg or www.sdic.org.sg).

In case of discrepancy between the English and Chinese versions, the English version shall prevail.

Information correct as at 1 December 2025.

GREAT Wealth Multiplier 3

Multiply your returns steadily to achieve your wealth goals and meet your lifestyle needs.

Let us match you with a qualified financial representative

Our financial representative will answer any questions you may have about our products and planning.