Why do newborns need an Integrated Shield plan

Why it makes sense to buy a private integrated shield plan for newborn child as early as possible.

For many of us, the days following the delivery of our newborn child will be remembered as some of the most hectic days of our lives. As parents, we are now responsible for the life of another human being – a person whose every need and want is ours to care for (and pay for!), at least in the next one to two decades.

As we adjust to this busy phase in our lives, there will be some important things we need to do. These include applying for birth registration, signing up for the baby bonus, and possibly planning for a 1-month or 100-day celebration.

For new parents, we like to suggest adding one more item to your to-do list, and that is to consider buying a private Integrated Shield plan for your newborn child.

Why getting a private Integrated Shield plan is necessary?

With so many things to do, it’s easy to procrastinate on things that are important but might seem less urgent. Getting the suitable insurance policies, however, is something that you should not delay.

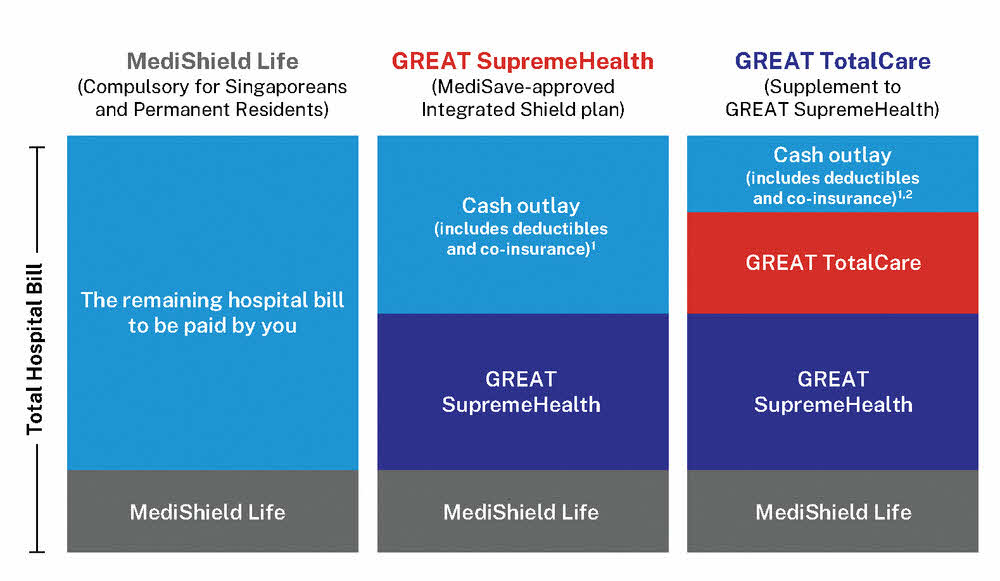

All Singapore citizens and Permanent Residents are covered by MediShield Life, a basic health insurance that offers lifetime protection against large hospital bills and selected costly outpatient treatments. MediShield Life is sized for subsidised treatment in public hospitals and pegged at Class B2/C-type wards.

However, MediShield Life coverage may not be sufficient for those with longer term medical conditions or with a preference for seeking treatment at private hospitals or at higher-class wards in restructured hospitals. For parents who want the best hospitalisation coverage that gives better choices for private hospitals and higher-class wards in restructured hospitals, many will choose to purchase a private Integrated Shield plan.

Pre-existing conditions are excluded by private insurers under an Integrated Shield plan. Since most newborn babies usually have a clean bill of health, this would be the best time to get them insured, as the insurers would likely accept the application with little to no exclusions.

The second risk is the probability of a newborn child being admitted to the hospital.

From my personal experience and observation, babies tend to fall sick easily. Due to their young age, doctors would err on the side of caution and may wish to admit an ill baby for hospital admission for further monitoring until the baby is better. However, once there is a hospital admission, we face a high likelihood of incurring a significant bill.

For example, when my oldest daughter was 3 months old, she was admitted to the hospital when she fell ill, while the hospital carried out some tests to rule out any serious infection. Thankfully, in my daughter’s case, she recovered and was discharged a few days later. However, even at a Class B1 ward in a public hospital, the bill came up to about S$1,500.

Thankfully, at that point, we’d already bought a private Integrated Shield plan for her, so we just needed to pay a minimum 5% co-payment.

Most medical insurance does not cover pre-existing conditions, any injuries or illnesses that affect you before you buy a new medical insurance plan.

Hence for a private Integrated Shield plan, it is wise to get it as early as possible when your newborn is healthy with no medical history. Once the policy is purchased, your child will receive the coverage as per the policy contract. If you only think about buying a private Integrated Shield plan after hospitalisation treatment is required, not only would that treatment not be covered, pre-existing illnesses will be excluded from coverage.

Generally, newborns with no medical history will most likely be able to get their application for their private Integrated Shield plan accepted.

However, once your newborn starts falling ill (as they inevitably will), a medical history may start forming. While most regular flu or virus infections are unlikely to lead to any medical concerns, all it takes is for a medical condition to develop and it may affect your private Integrated Shield plan application.

Even if parents know that the hospital admission wasn’t for anything serious or that there are no long-term health issues that their child has, we can expect the insurance companies to ask for further information in order to assess the application. This assessment process can mean more time taken to get your child covered, even if it does not lead to any exclusions.

For parents looking for a private Integrated Shield plan to cover their newborn, the GREAT SupremeHealth is an example of a MediSave-Approved Integrated Shield Plan that can be considered.

When GREAT SupremeHealth is complemented with the supplement rider GREAT TotalCare, up to 95% of the total hospitalisation bill can be covered.

Furthermore, the 5% co-payment is capped at a limit of S$3,000 every policy year, for the eligible bills incurred under Panel Provider or at Restructured Hospital.

For those who are worried about the gap in coverage for the first 14 days after birth, or even before your baby is delivered, you can consider a maternity insurance plan such as the GREAT Maternity Care 2.

With a one-time premium, the GREAT Maternity Care 2 can provide coverage as early as 13 weeks of pregnancy, with coverage extending until the end of the third policy year. This coverage applies to both child and mother, covering 18 pregnancy and childbirth complications as well as against 26 congenital conditions that a child may have from birth.

Similar to getting a private Integrated Shield plan, it would also make sense for expecting mothers to get the GREAT Maternity Care 2 as early as possible in the pregnancy to maximise the coverage received. This is because you will be paying the same one-time premium for the policy, regardless of whether the policy is bought during the early stage (week 13 and onwards) or later stage (before week 36) of the pregnancy.

As parents of newborns, there will be many milestones that we can look forward to. These include the day they are born, the day they are discharged from the hospital and their first birthday.

Even as we celebrate these milestones in their lives, let’s not forget to ensure they have adequate insurance protection and to get the suitable policies. Remember, the sooner they are covered, the earlier they can benefit from the additional medical coverage if medical emergencies happen.

Disclosure: This article is written by Timothy Ho, a writer and is in collaboration with Dollars and Sense.

GREAT SupremeHealth

Enhanced with GREAT TotalCare and cover up to 95% of your hospitalisation bill

Footnotes

1 The deductible is the amount which must be borne by the policyholder before any benefit becomes payable under GREATSupremeHealth. Co-insurance is the proportion of the expenses that needs to be borne by the policyholder after the deduction of the deductible (where applicable).

2 95% of the deductible is covered under selected GREAT TotalCare plan types. Please refer to Benefit Table in the policy contract for more information on coverage of the deductible under the different GREAT TotalCare plans.

Source

* The Co-payment shall be subject to a maximum of $3,000 per Period of Insurance for the Eligible Bills incurred (a) under Panel Provider or at Restructured Hospital covered under GREAT SupremeHealth; (b) under Panel Provider or at Restructured Hospital for Additional Cancer Support covered under GREAT TotalCare, and/or (c) where the Life Assured was admitted as a result of an Emergency. For the avoidance of doubt, where the Company determines that the admission does not constitute an Emergency, the cap shall not apply. The cap also does not apply to all Expenses incurred for Outpatient Cancer Drug Treatment not on the Cancer Drug List.

Terms and conditions apply. Please refer to the policy contracts for the full conditions of the policies. This advertisement has not been reviewed by the Monetary Authority of Singapore.

GREAT TotalCare is not a MediSave-approved Integrated Shield plan and premiums are not payable using MediSave. GREAT TotalCare is designed to complement the benefits offered under GREAT SupremeHealth. As these products have no savings or investment feature, there is no cash value if the policy ends or is terminated prematurely.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The information presented is for general information only and does not have regard to the specific investment objectives, financial situation or particular needs of any particular person.

Protected up to specified limits by SDIC.

Information correct as at 13 October 2023.

Let us match you with a qualified financial representative

Our financial representative will answer any questions you may have about our products and planning.