3 things to do in your 30s

Get financial independence with insurance coverage at lower premiums for better later years.

Hearing popular songs from the 2000s now playing on Gold 90.5, and seeing all your friends getting hitched or popping out babies.

If you’ve experienced this, welcome to your 30s. Congrats on surviving 3 decades of your life, going through school, graduating and getting your career off the ground.

From getting married and planning to buy a new HDB BTO flat to making big strides in your career or perhaps even starting a business, there are lots of new and exciting milestones in life that we are just about to hit or have just achieved.

One constant, however, is that we are approaching our later years — it’s time to sit up and take notice of things like our health and plan for our financial future. But the benefit of being in our 30s is that we still have time on our side to pave the way for a more comfortable life when we get older. The key thing is to start now.

Here are 3 things to do in your 30s to make your later years much better:

Kick bad habits and lead a healthy lifestyle

Trust us, your body will thank you later.

Once you reach your 30s, your metabolism starts to slow down. If you are the type who used to be able to eat everything and still not gain weight, it may be time to re-evaluate your diet and lifestyle choices so that you reduce the risk of heart problems or chronic diseases such as diabetes or high cholesterol as you age.

Simple things like cooking more and swapping out unhealthier ingredients for healthier alternatives, introducing more vegetables to your diet, and overindulging less are easy enough to ease into.

You may also wish to get a gym membership to motivate you to exercise regularly or buy an affordable bicycle of your own.

Needless to say, bad habits like smoking and over drinking are not activities that should be part of your life if you want to reduce your risk of health problems in the future.

Build up your financial independence

As you’re hitting all these new milestones in life — getting married, renovation for a new house, preparing to have a child — you are spending lots of money and likely accumulating debt.

All these commitments mean that if you encounter any unexpected mishaps, sudden illness or disability, you may suffer a loss of income and incur more expenses especially if you need help in your day-to-day activities.

Long-term care costs incurred due to disability can take out a significant chunk of one’s savings and one way to avoid depleting your savings under such a situation is to insure yourself early with long-term care insurance plans. While the Government’s CareShield Life scheme helps, the starting monthly payout of S$600 in 2020 may not be enough. Also, only those who are suffering from a severe disability* are eligible for this monthly payout.

You’ll want a plan that adequately covers you — even for a mild disability* — and one where you can utilise your MediSave funds. That’s why private insurers such as Great Eastern offer CareShield Life supplementary plans.

Under Great Eastern’s GREAT CareShield, those with a mild disability* — in which they are unable to perform 1 out of the 6 Activities of Daily Living3 (ADLs): washing, toileting, dressing, feeding, walking or moving around, and transferring — can get a lump sum payout and monthly benefit of 50% (up to S$2,500)§. Their future premiums will also be waived for as long as the insured person remains disabled (unable to perform at least 1 ADL)ǁ.

Should the insured person’s disability worsen from mild to moderate*, or even to severe disability*, the monthly benefit payout of up to S$5,000/month continues and they will also be eligible to receive payouts from the Government’s CareShield Life scheme, starting from S$600/month in 2020. In addition, GREAT CareShield also provides a Caregiver Benefit4 (60% of monthly benefit or up to S$3,000 for up to 12 months) and a Dependant Care Benefit5 (30% of monthly benefit or up to S$1,500 for up to 48 months).

Here’s a look at the available CareShield Life supplement plans offered by Great Eastern's GREAT CareShield:

| Plan Type | GREAT CareShield |

|---|---|

| Selectable Monthly Benefit | Minimum: S$300 / Maximum: S$5,000 (in multiples of S$10) |

| Initial Benefit2 | One lump sum of 3 times the Monthly Benefit payable upon inability to perform only 1 ADL |

| Monthly Benefit1 | 50% of Monthly Benefit payable upon inability to perform only 1 ADL; 100% of Monthly Benefit payable upon inability to perform at least 2 ADLs |

| Caregiver Benefit4 | 60% of Monthly Benefit payable upon inability to perform at least 2 ADLs, for up to 12 months |

| Dependant Care Benefit5 | 30% of Monthly Benefit payable upon inability to perform at least 2 ADLs, for up to 48 months |

| Waiver of Premium7 | Premiums are waived upon inability to perform at least 1 ADL |

| Policy Term | Lifetime |

| Premium Type | Level premium based on age last birthday at entry |

| Premium Payment Term |

|

Here's how it works:

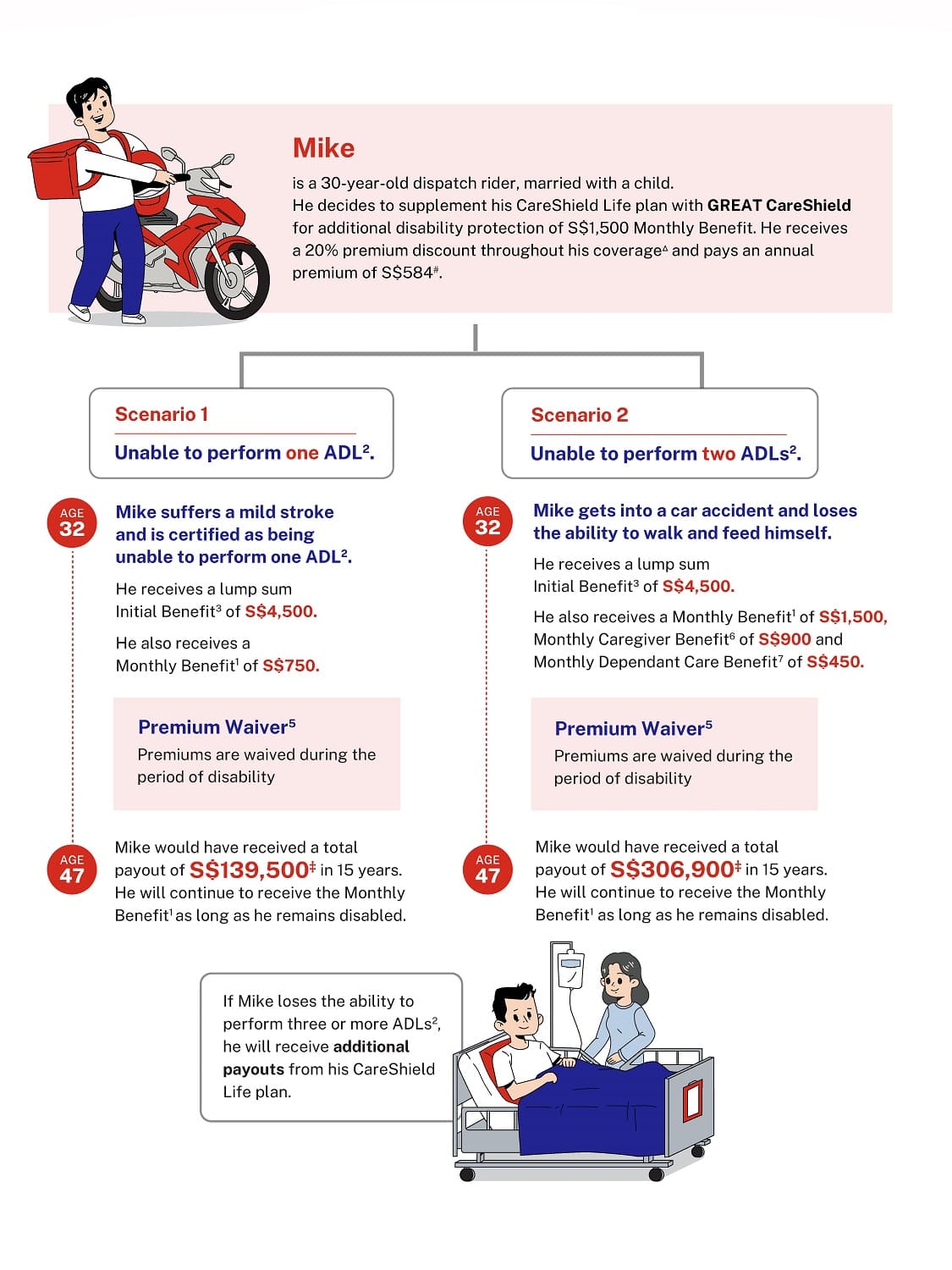

Take 30-year-old Mike, who signs up for GREAT CareShield, with a premium payment term of up to age 95.

He pays an annual premium of S$584†, which is fully payable via MediSave for a monthly benefit of S$1,500.

At age 40, Mike suffered from a mild stroke and was diagnosed as suffering from the inability to perform 1 ADL:

Initial Benefit2

He receives a lump sum payout of S$4,500 to help in his purchase of equipment to aid his disability.

Monthly Payout1

He also starts to receive a monthly payout of S$750 (50% of the monthly benefit) to supplement any loss of income due to his disability.

Premium waiver7

Premiums are waived during this period of mild disability.

Mike fully recovers after 1 year at the age of 41.

At age 45, Mike gets into an accident and was diagnosed as suffering from the inability to perform 2 ADLs:

Initial Benefit2

He receives a lump sum payout of S$4,500 to help in his purchase of equipment (e.g. wheelchair/crutches etc.) Note: this is payable again as the second disability is different from the first.

Monthly Payout1

He also starts to receive a monthly payout of S$1,500 to hire a live in caregiver.

Caregiver benefit4

The caregiver benefit will pay out S$900 per month (60% of monthly benefit) for up to 12 months so as to help his partner/family member to tide them over this 1-year period which they help train the live-in caregiver on how to take care of Mike and for Mike to get used to his new lifestyle.

Dependant Care benefit5

As Mike has a child under the age of 22, he also receives an extra S$450 per month for up to 48 months.

Premium waiver7

Premiums are waived during this period of moderate disability.

Upon his inability to perform 3 ADLs, Mike receives payouts from GREAT CareShield in addition to his CareShield Life payouts.

Mike was able to use his MediSave to pay for his annual premiums, there is no cash outlay required — great news for those of us with growing financial commitments!

Start early as your premiums do not increase with age

As with all insurance plans, it’s best to get started early. What this means is, when Mike purchases GREAT CareShield, he can:

- Go for a higher payout at a lower premium

- He can be paying the same premium year on year as the premium amount does not increase with his age‡. This means that Mike will be paying S$584† annual premium using his MediSave now for a monthly benefit of S$1,500.

Set your sights afar and prepare yourself for the unexpected

How many of us in our 30s think about diseases that may hit us when we’re older? Not often I bet, but the unpredictability of life hits us when we see parents or relatives grappling with diseases or medical conditions.

According to a local study done in 2019, the proportion of older adults with 3 or more chronic diseases nearly doubled from 2009 to 2017, and stroke/high blood pressure and diabetes are among the most common chronic health conditions in Singapore.

Stroke/high blood pressure

According to the Singapore Stroke Registry Annual Report 2018 by the National Registry of Diseases Office, the number of stroke episodes has increased over the years (5,760 episodes in 2009 to 8,326 episodes in 2018; incidence rate also increased significantly from 187.9 per 100,000 population in 2009 to 244.7 per 100,000 population in 2018). The report also found that over the past decade, there was also a significant rise in incidence rates for the 15-29 years, 40-49 years, and 50-59 years age groups.

Though the statistics from the Ministry of Health show that deaths from stroke have decreased over the years, this possibly means that there are more stroke survivors, with some suffering from some forms of disability and needing long-term care. Also, it is good to know that one of the common risk factors for stroke is hypertension (high blood pressure), which affects almost a quarter of Singapore residents aged 30 to 69 years.

Diabetes

Oh, bubble tea, Instagram-worthy dessert shops and ice-cream parlours with all sorts of delectable flavours… With so much sugar in our system, it’s no wonder that an estimated 19,000 people are diagnosed with Type 1 or Type 2 diabetes each year. According to the Ministry of Health statistics, the prevalence of diabetes among those aged 18 to 69 years increased from 7.3% in 1992 to 8.6% in 2017.

Diabetes is more than just high blood sugar. If left uncontrolled, diabetes can damage blood vessels and affect multiple organs in the body and increase the risk of developing gangrene which may lead to loss of limbs.

In a 2016 report by the National Healthcare Group, it said that Singapore has one of the highest rates of lower extremity amputation in the world. Diabetes can also affect vision and may lead to blindness.

In less severe cases of amputation and vision loss, one may still be able to perform their day-to-day activities independently. If it is assessed to be mild disability where one cannot perform 1 Activity of Daily Living, he/she will not receive any payout from the Government’s CareShield Life scheme. However, with the GREAT CareShield, one will receive a lump sum payout of up to S$15,000‡. Under this CareShield Life supplement, one can also receive up to lifetime monthly payout of 50% of the monthly benefit upon 1 ADL (subject to deferment period and for as long as the life assured suffers from 1 ADL). If the disability becomes severe (unable to perform at least 3 ADLs), they’d be entitled to both GREAT CareShield and the Government’s CareShield Life monthly payouts6.

The burden of chronic medical conditions

Chronic medical conditions require long-term treatment and medication which can be costly. In addition, there may be other costs, such as enrolling yourself into a nursing home, hiring a live-in caregiver, retrofitting the house to make it more disabled-friendly, or even having a family member quit their job to be a full-time caregiver.

In addition, according to the Ministry of Social and Family Development, about 3.4% of Singapore Citizens and permanent residents aged 18 to 49 were disabled in 2018. That’s over 130,000 people.

There are also limits to how much your MediSave and MediShield Life can cover. Also, if you haven’t bought insurance and you get diagnosed with a chronic disease, you may not be able to get insured for it later.

Another unexpected mishap that could happen regardless of age is disability. In fact, the most common causes of disabilities in Singapore are due to accidents, illness or old age. Being young does not protect you from disabilities.

Statistics from the Ministry of Social and Family Development show that the percentage of persons with disabilities increases nearly four-fold with age.

On top of costs of medical treatment and long-term care, you may still have to continue supporting your family even if you were caught in an accident.

Just remember, it’s good to always be financially prepared for what life throws at us. Being in your 30s, you’ve still got time on your side to ensure your later years go smoother. So go on, get adequately covered, then go out and live it up in your roaring 30s!

Footnotes:

1 Subject to Deferment period. Payouts of Monthly Benefit are payable for as long as the Life Assured suffers from the applicable number of disabilities, up to a lifetime.

2 The Initial Benefit is a lump sum payment equivalent to 3 times of the Monthly Benefit. In the event the Life Assured fully recovers from the disability, the Initial Benefit may be paid again for subsequent episodes of inability to perform at least 1ADL. However, it is not payable if such subsequent disabilities arise from or are related to the cause of disability(ies) for which there was a previous claim for Initial Benefit.

3 Activities of Daily Living (ADLs) are: washing, toileting, dressing, feeding, walking or moving around and transferring.

4 Subject to Deferment Period and payable for up to a maximum of 12 months (whether consecutive or not) per Policy Term.

5 Applicable if the Life Assured has a Child who is below 22 years old (age last birthday) as at the Claim Date; subject to Deferment Period and payable for up to a maximum of 48 months (whether consecutive or not) per Policy Term.

6 The Monthly Benefit supplements your CareShield Life monthly payouts which start from S$600 in 2020.

* Mild disability means your inability to perform one ADL and will require significant assistance from another person when carrying out the activity. Moderate disability means your inability to perform two ADLs and will require significant assistance from another person when carrying out the activities. Severe disability means your inability to perform at least three ADLs and will require significant assistance from another person when carrying out the activities. Subject to Deferment Period and “mild disability” is the inability to perform 1 Activity of Daily Living (ADL).

ǁ Subject to Deferment Period, and for as long as he continues to suffer from the disability.

§ Subject to Deferment Period and “mild disability” is the inability to perform 1 Activity of Daily Living (ADL). The Initial Benefit is a lump sum payment equivalent to 3 times of the Monthly Benefit. In the event the Life Assured fully recovers from the disability, the Initial Benefit may be paid again for subsequent episodes of mild disability. However, it is not payable if such subsequent disabilities arise from or are related to the cause of disability(ies) for which there was a previous claim for Initial Benefit.

† Premiums are rounded down to the nearest dollar.

‡ Premium rates are not guaranteed and they may be adjusted from time to time based on future experience.

All payouts are subject to the Deferment Period. Payouts are payable for as long as the life assured suffers from the applicable number of disabilities, up to the life assured’s lifetime.

Terms and conditions apply. Protected up to specified limits by SDIC.

The information presented is for general information only and does not have regard to the specific investment objectives, financial situation or particular needs of any particular person.

This is only product information provided by Great Eastern. You may wish to seek advice from a qualified adviser before buying the product. If you choose not to seek advice from a qualified adviser, you should consider whether the product is suitable for you. Buying health insurance products that are not suitable for you may impact your ability to finance your future healthcare needs.

If you decide that the policy is not suitable after purchasing the policy, you may terminate the policy in accordance with the free-look provision, if any, and the insurer may recover from you any expense incurred by the insurer in underwriting the policy.

Information correct as at 15 March 2024.

Source: MoneySmart. Permission required for reproduction.

Let us match you with a qualified financial representative

Our financial representative will answer any questions you may have about our products and planning.