Maternity Protect Series

Maternity Protect Series | Pregnancy and Newborn Insurance

Protection that grows with your family, from bump to beyond.

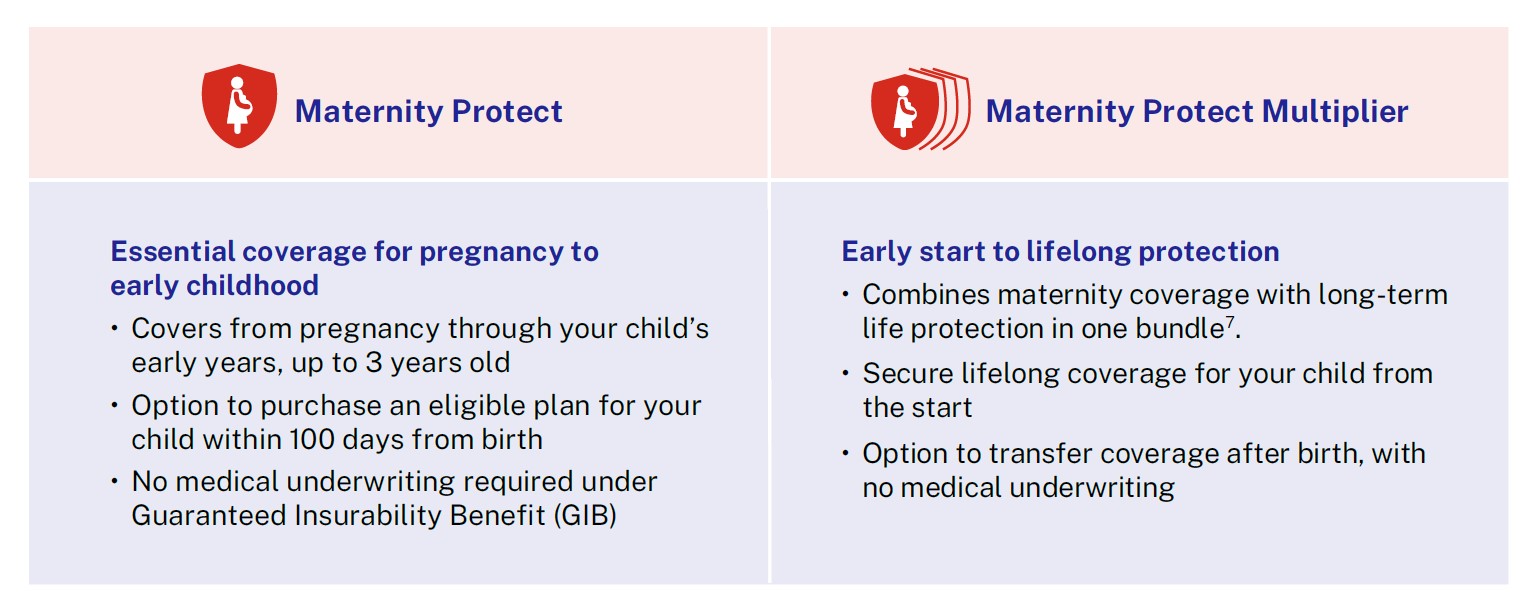

The Maternity Protect Series cares for you through pregnancy, childbirth, and gives you the flexibility to plan ahead for your child, with options to provide continuity of protection in the years to come.

Key benefits

-

Care for mum, from delivery to recovery

Covers 18 pregnancy and childbirth conditions¹, including hospital cash² for 27 specified conditions. Receive an additional payout for early C-sections³. Plus, emotional wellbeing support⁴, as well as coverage for future pregnancies through the Mum Again benefit.

-

Protection for your child’s early years

Covers congenital and juvenile conditions⁵, with daily hospital cash* and developmental delay benefits⁶, so you can focus on your child’s care.

-

Guarantee your child's lifelong protection from the very start

Start your child’s coverage early when bundled with GREAT Life Multiplier7, with options to transfer protection without medical underwriting, when exercised within 100 days post birth8. Enjoy coverage even if the condition or medical procedure is linked to a pre-existing condition9.

-

Support when income is disrupted

Receive a one-time cash payout of up to S$5,000* if either parent is retrenched10.

Choose the plan that suits your needs

Your questions answered

Q1: What is Maternity Protect and how does it support me and my baby?

A1: Maternity Protect is a 3‑year, single‑premium, non‑participating maternity term plan that provides insurance coverage for the mother (life assured) and her insured child(ren).

You may apply for this plan if you are between 13 and 36 weeks of pregnancy at the time of application.

The plan provides coverage at different stages, subject to the terms and conditions of the policy:

• During pregnancy and delivery (mother):

Coverage includes death or total and permanent disability (TPD), pregnancy and childbirth complications, hospital care, psychological consultations, and early delivery by caesarean section.

• After birth (child):

Coverage includes death, congenital illnesses and juvenile illnesses, hospital care, surgery on any of the five major organs (heart, lungs, liver, kidneys or brain) and developmental support.

Q2: What benefits are covered under Maternity Protect?

A2: Maternity Protect provides coverage for both mother and child, across pregnancy, childbirth, and early childhood.

Each benefit is subject to its applicable benefit limit and coverage period.

Benefits will cease when the applicable limit is reached, the coverage period ends, or where the benefit is payable once, upon an admitted claim under that benefit, unless otherwise stated.

Members |

Benefits |

Benefit Limit and Expiry |

Life Assured (Mother) |

Death or Total and Permanent Disability (TPD) Benefit |

100% of the Basic Sum Assured, payable once. Covers up to the end of the policy term. |

Pregnancy and Childbirth Complications Benefit |

100% of the Basic Sum Assured, payable once. Ends 120 days from the date of birth of the insured child. |

|

Hospital Care Benefit |

2% of the Basic Sum Assured is payable per day, up to a maximum of 30 days. Ends when the 30-day limit has been reached, or 120 days from the date of birth of the insured child, whichever comes earlier. |

|

Psychological Consultations Benefit |

S$100 per session, up to a maximum of 3 sessions. Ends once the maximum number of sessions has been reached or 120 days from the birth of the insured child, whichever comes earlier. |

|

Early Delivery by Caesarean Section Benefit |

15% of the Basic Sum Assured, payable once, subject to the policy terms and conditions. Ends upon an admitted claim under this benefit or the birth of the insured child, whichever occurs earlier. |

|

Mum Again Benefit |

This option allows the life assured to purchase one eligible maternity plan with similar benefits, on her own life for a subsequent pregnancy, without medical underwriting, subject to the policy terms and conditions. |

|

Insured Child(ren) |

Death Benefit |

100% of the Basic Sum Assured, payable once. Covers up to the end of the policy term. |

Congenital Illness Benefit |

100% of the Basic Sum Assured, payable once. Covers up to the end of the policy term. |

|

Juvenile Illness Benefit |

100% of the Basic Sum Assured, payable once. Covers up to the end of the policy term. |

|

Hospital Care Benefit |

2% of the Basic Sum Assured per day, up to a maximum of 30 days. Ends when the 30-day limit has been reached, or at the end of the policy term, whichever comes earlier. |

|

Major Organ Benefit |

50% of the Basic Sum Assured is payable once. Covers up to the end of the policy term. |

|

Developmental Support Benefit |

Reimbursement of eligible therapy expenses of up to S$200 per session, subject to an aggregate cap equal to the lower of 15% of the Basic Sum Assured or S$3,000, covers up to the end of the policy term, subject to the policy terms and conditions. |

|

Guaranteed Insurability Benefit |

This option allows the policyholder to purchase an eligible insurance plan for the insured child, made available by us from time to time at our discretion, without medical underwriting, subject to the policy terms and conditions. |

|

Parents |

Parental Retrenchment Cash Benefit |

20% of the Basic Sum Assured, payable once during the policy term on a first-to-claim basis, regardless of whether the claimant is the mother or the other parent, subject to the policy terms and conditions. |

For full detailed terms and conditions on termination, you are advised to read the policy contract.

Q3: What happens if I am pregnant with multiple babies?

A3: Maternity Protect provides coverage for up to two foetuses (twins) in the same pregnancy.

Each child will be covered separately. Where a benefit has been paid for one insured child, the same benefit may, unless otherwise stated, still be available for the other insured child, in accordance with the policy.

Q4: Is assisted pregnancy covered under Maternity Protect?

A4: Maternity Protect covers pregnancies that result from natural conception, as well as pregnancies conceived through the following assisted fertility treatments:

(a) In Vitro Fertilisation (IVF);

(b) Intracytoplasmic Sperm Injection (ICSI);

(c) Intrauterine Insemination (IUI); and

(d) Intracervical Insemination (ICI).

Coverage is subject to the terms and conditions of the policy.

Pregnancies and related complications arising from any other fertility treatments are not covered under this plan.

Q5: Will my policy end after a claim is paid?

A5: No. Each benefit is payable up to its applicable benefit limit or coverage period. After a claim is paid under one benefit, the remaining applicable benefits will continue unless otherwise stated.

The policy will terminate only when:

(a) the policy term expires;

(b) all benefits under the policy have been paid up to their applicable benefit limits;

(c) the Death Benefit for the life assured and all insured child(ren) are paid; or

(d) the policyholder requests termination.

If Maternity Protect is purchased together with GREAT Life Multiplier, the two policies are issued separately. Claims made under one policy will not affect the continuation of the other policy, subject to the terms and conditions of each policy.

As this product has no savings or investment feature, there is no cash value if the policy ends or is terminated early.

Q6: What is Mum Again Benefit?

A6: The Mum Again Benefit allows an eligible life assured (mother) to purchase a subsequent eligible maternity plan with similar benefits made available by us from time to time, without medical underwriting for her next pregnancy, subject to the following conditions:

(a) the current Maternity Protect policy has been medically underwritten;

(b) the option must be exercised within 5 years from the commencement date of the medically underwritten policy;

(c) no claim was made on the life assured under the current policy; and

(d) at the point of exercising the option, the life assured:

(i) is between 18 to 40 years of age next birthday;

(ii) has a pregnancy that is at less than or equal to 16 weeks of gestation;

(iii) conceived naturally with no more than 2 foetuses; and

(iv) where pre‑natal genetic or other medical tests have been conducted, no adverse or abnormal findings relating to the pregnancy or foetus have been identified or communicated to the life assured.

Q7: What is the Guaranteed Insurability Benefit (GIB) option?

A7: The Guaranteed Insurability Benefit (GIB) allows the policyholder to purchase an eligible insurance plan for the insured child without medical underwriting, subject to the terms and conditions of the policy.

Eligible plans made available by us from time to time may provide one or more of the following benefits:

(a) Death benefit;

(b) TPD benefit;

(c) Terminal illness benefit; and/or

(d) Critical illness benefit

The GIB option must be exercised within 100 days from the birth of the insured child, and may be exercised once for each insured child, subject to policy terms. Eligible plans and maximum sums assured are determined by us and may change from time to time.

This option applies to the insured child only.

When Maternity Protect is purchased together with GREAT Life Multiplier, only one option — either the GIB or the Transfer of Life (TOL) option — may be exercised for the insured child.

Any insurance policy purchased under the Guaranteed Insurability Benefit (GIB) is subject to its own terms and conditions, including how pre‑existing conditions are defined and treated.

Please refer to the policy contract for full details, including applicable terms, conditions and exclusions.

Q8: My child has a condition detected after birth. Will it be covered under a new plan purchased using the Guaranteed Insurability Benefit (GIB)?

A8: If you purchase a new insurance plan for your child using the Guaranteed Insurability Benefit (GIB), conditions diagnosed before the start of the new policy may be covered, subject to the terms and conditions of that policy.

For conditions that are related to a pre-existing condition and diagnosed before your child reaches 6 years old, the total payouts are capped at S$30,000 per child and are payable once only.

After a payout is made, the policy will continue with any remaining coverage, where applicable, subject to the policy terms and conditions.

Please refer to the policy contract of the new insurance plan for full details, including applicable terms, conditions, benefit limits and exclusions.

Q9: What happens if I surrender my Maternity Protect policy early?

A9: All coverage under the policy will cease if the policy is surrendered early. As this plan has no savings or investment feature, there is no cash value upon early termination.

Q10: What happens when Maternity Protect is purchased together with GREAT Life Multiplier?

A10: When Maternity Protect is purchased together with GREAT Life Multiplier:

• Two separate policies are issued;

• Maternity Protect benefits remain unchanged;

• The Transfer of Life option becomes available under the GREAT Life Multiplier policy; and

• For multiple babies (e.g. twins), a separate GREAT Life Multiplier policy will be issued for each insured child, subject to policy terms.

Each policy operates independently and has its own benefits, terms and claims assessment.

Q11: What is the Transfer of Life (TOL) option?

A11: The Transfer of Life (TOL) option allows the policyholder to transfer the coverage under the GREAT Life Multiplier policy from the life assured to the insured child, subject to the terms and conditions of the policy.

This option is available only when GREAT Life Multiplier is purchased together with Maternity Protect.

Q12: Can both the Transfer of Life (TOL) option and the Guaranteed Insurability Benefit (GIB) be exercised?

A12: No. Only one option may be exercised for the insured child:

• GIB option (under the Maternity Protect policy), or

• TOL option (under the GREAT Life Multiplier policy).

Once one option is exercised, the other will no longer be available.

Q13: When can the Transfer of Life (TOL) option be exercised?

A13: The TOL option may be exercised any time before the 1st policy anniversary. If the TOL option is exercised within the first 100 days of the child’s date of birth, no medical underwriting will apply.

After the 100‑day period, medical underwriting will apply.

Q14: Is there a minimum age for my child to exercise the TOL option?

A14: No. The TOL option may be exercised once the child is born, subject to terms and conditions set out in the policy.

Q15: What happens if the TOL option is not exercised?

A15: If the TOL option is not exercised, the GREAT Life Multiplier policy will continue to cover the life assured, and the insured child will not be covered under that policy.

Q16: What happens to my policy after the TOL option is exercised?

A16: After a successful exercise of the TOL option:

• the insured child becomes the new life assured under the GREAT Life Multiplier policy;

• all rider(s), except any accelerating CI rider(s) providing coverage for the original life assured will be terminated;

• any loadings imposed on the original life assured will be removed from the effective date of transfer; and

• the basic sum assured of the GREAT Life Multiplier policy will revised to the insured child’s basic sum assured (as set out in the policy illustration).

Q17: If my child has a condition detected after birth, how will it be treated under the Transfer of Life (TOL) option?

A17: When the Transfer of Life (TOL) option is exercised, your child becomes the life assured under the existing GREAT Life Multiplier policy.

Any condition your child has within the first 100 days of his/her life will be considered a pre-existing condition according to the policy’s definition.

For certain benefits, such as critical illness riders, if the condition is related to a pre‑existing condition and occurs before age 6, the total payout is capped at S$30,000 and payable once only, in accordance with the policy terms and conditions.

All other benefits will continue to be assessed based on the policy terms and conditions.

Please refer to the GREAT Life Multiplier policy (including the Transfer of Life (TOL) endorsement) for full details, including applicable terms, conditions and exclusions.

Q18: What is the difference between the GIB option and the TOL option for my child?

A18: The Guaranteed Insurability Benefit (GIB) option allows you to buy a new insurance plan for your child without medical underwriting, subject to policy terms and the eligible plans available at the point of exercising the option.

The Transfer of Life (TOL) option allows you to transfer the existing GREAT Life Multiplier policy from the mother to your child.If Maternity Protect is purchased on its own, only the GIB option is available.

If it is purchased together with GREAT Life Multiplier, you can choose either the GIB option or the TOL option.

Please refer to the Maternity Protect policy and the GREAT Life Multiplier policy (including the Transfer of Life (TOL) endorsement) for full details, including applicable terms, conditions and exclusions.

Q19: If my baby has a pre‑existing condition, will it be covered under hospitalisation plans purchased under the campaign?

A19: No. Pre-existing conditions will not be covered under hospitalisation plans purchased under the campaign.

Pre-existing Condition refers to:

(a) any illness, disease, disability, defect or impairment from which the life assured was suffering prior to the commencement date of insurance; or

(b) any illness, disease, disability, defect or impairment of which signs or symptoms had existed in the 12 months immediately preceding the commencement date of insurance, for which:

(i) the life assured had sought or received medical advice or treatment, prescription of drugs, counselling, investigation or diagnostic tests, surgery, hospitalisation; or

(ii) an ordinarily prudent person would have sought medical advice or treatment, prescription of drugs, counselling, investigation or diagnostic tests, surgery, hospitalisation.

Q20: If my baby is born early or has a health issue or pre-existing condition, can I still apply for a hospitalisation plan for my baby under the campaign?

A20: No. You will not be able to apply for a hospitalisation plan under the campaign if your baby:

• is born before 37 weeks of gestation; or

• has a health issue or pre-existing condition.

However, you may still apply for a hospitalisation plan for your baby, subject to full medical underwriting and acceptance by us.

Q21: How many hospitalisation plans can I purchase for my baby if I am eligible for the campaign?

A21: If you are eligible under the campaign, you may purchase any of the Qualifying Plans listed below for your baby without medical underwriting. The list of Qualifying Plans may be updated from time to time by us.

Qualifying Plans (as at 9 June 2026):

• GREAT SupremeHealth P Prime NEW

• GREAT SupremeHealth A Plus

• GREAT SupremeHealth B Plus

• GREAT SupremeHealth Standard

• GREAT TotalCare 2 Prime NEW

• GREAT TotalCare 2 A

• GREAT TotalCare 2 B

• GREAT TotalCare Plus 2 Essential

• GREAT Hospital Cash Plan A

• GREAT Hospital Cash Plan B

Please refer to the Campaign Terms and Conditions for full details.

Q22: Am I eligible for this campaign if I purchased GREAT Maternity Care 2 policy instead of Maternity Protect?

A22: Yes. You will be eligible for this campaign if you have an in‑force GREAT Maternity Care 2 or Maternity Protect policy, subject to the campaign’s terms and conditions.

To qualify, your baby must:

• be covered under an in-force GREAT Maternity Care 2 or Maternity Protect policy and be the proposed life assured under the Qualifying Plan(s);

• be born at or after 37 weeks of gestation;

• be at least 15 days old and discharged from the hospital; and

• be no more than 100 days old at the point of application.

Q23: If I purchase a new hospitalisation plan for my baby under this campaign, can I later upgrade to another qualifying plan using the simplified application?

A23: No. The simplified application applies only to the purchase of a new qualifying plan under this campaign.

It does not apply to any subsequent upgrade to an existing plan after purchase, even if the upgraded plan is also a qualifying plan under the campaign.

Let our Financial

Representative serve you

We are happy to help you.

Understand the details before buying

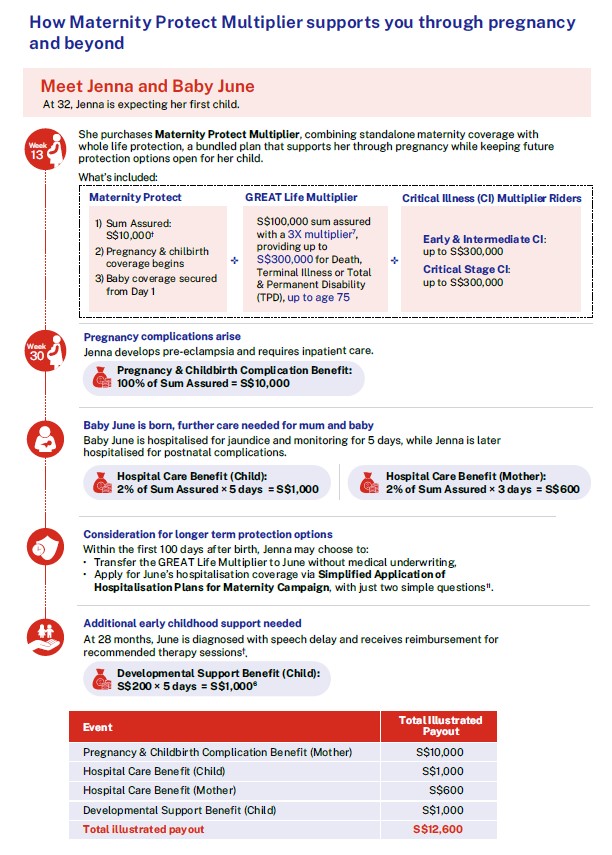

1 If the life assured (mother) is pregnant with more than 1 foetus in the same pregnancy, the Pregnancy and Childbirth Complications Benefit is payable once per pregnancy. 2 The Hospital Care Benefit is payable for up to 30 days in total. For the life assured (mother), it ends when 30 days are reached or 120 days after birth, whichever is earlier. For each insured child, it ends when 30 days are reached or at the end of the policy term, whichever is earlier. If there is more than one foetus, the benefit is payable separately for each insured child. 3 Under the Early Delivery by Caesarean Section Benefit, 15% of the basic sum assured is payable if the delivery is by caesarean section that is certified to be medically necessary, performed before 36 weeks of gestation, and applies to singleton pregnancies only. This benefit is payable once per pregnancy. 4 Under the Psychological Consultations Benefit, S$100 is payable per session, up to 3 sessions. The benefit ends when the maximum sessions are used or 120 days after birth, whichever is earlier. 5 An insured child refers to each biological child covered under the policy, and benefits are payable once per insured child. If there is more than one foetus, each insured child will be covered separately. Where a benefit has been paid for one insured child, the same benefit may still be payable for another insured child, unless otherwise stated. 6 Under the Developmental Support Benefit, eligible developmental support therapy expenses are reimbursed up to S$200 per session, capped at the lower of 15% of the basic sum assured or S$3,000 per insured child. 7 GREAT Life Multiplier (and any riders, if applicable) is a separate policy from Maternity Protect, and all benefits are subject to the terms and conditions of the respective policies. 8 The Guaranteed Insurability Benefit (GIB) can be exercised once within 100 days from birth to purchase eligible plans for the child, subject to limits set by Great Eastern, and excluding hospitalisation plans such as GREAT SupremeHealth and GREAT TotalCare. The list of eligible plans and maximum sum assured may be revised by Great Eastern, and full terms and conditions are set out in the policy contract. The Transfer of Life (TOL) option can be exercised once before the first policy anniversary. No medical underwriting is required if exercised within 100 days from birth of the insured child, and medical underwriting will apply thereafter. The policyholder may choose either the GIB or TOL option based on their intended coverage needs, subject to policy terms and conditions. 9 If the insured child is diagnosed with a covered condition or undergoes a covered medical procedure which is caused directly or indirectly by a pre-existing condition, before the policy anniversary on which the insured child is 6 years old, we will pay out the claim subject to a cap of S$30,000 and only one such claim will be admitted. 10 The Parental Retrenchment Cash Benefit is payable once during the policy term on a first-to-claim basis, subject to eligibility conditions, waiting periods, exclusions, and policy terms. 11 For the Simplified Application of Hospitalisation Plans for Maternity Campaign, the child must be born at or after 37 weeks of gestation, be at least 15 days old and discharged from hospital, and be no more than 100 days old at the point of application. Pre‑existing conditions will not be covered. Terms and conditions apply. * Benefit amounts illustrated are based on a basic sum assured of S$25,000. † Illustrated payouts are for illustrative purposes only and actual benefits depend on the selected basic sum assured and policy terms. |

All ages specified refer to age next birthday.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The above is for general information only. It is not a contract of insurance. The precise terms, conditions and exclusions of this insurance plan are specified in the policy contract.

As Maternity Protect has no savings or investment feature, there is no cash value if policy ends or is terminated prematurely.

These policies are protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC websites (www.lia.org.sg or www.sdic.org.sg).

Information correct as at 9 June 2026.